On January 28, 2021, at the peak of the GameStop squeeze, Robinhood turned off the buy button. Users could sell GME, AMC, and a handful of other meme stocks, but they could not open new positions. Robinhood pointed to clearinghouse collateral requirements, which was a real constraint. But the image stuck: a brokerage that restricted trading in the one direction that would have hurt its counterparties, at the exact moment its users wanted in. Vlad Tenev ended up testifying before Congress. The phrase “buy button” became shorthand for a platform that could unilaterally decide who trades what, and when.

Five and a half years later, the same company has launched a public blockchain and put the word “permissionless” on the front of it.

That contrast is the right place to start, because the interesting question about Robinhood Chain is not whether the technology works. It almost certainly does. The question is what it means for a company with Robinhood’s history and business model to operate rails it describes as open, and whether the flagship asset those rails were built for is nearly as open as the chain underneath it.

This piece reflects the state of things as of July 2, 2026, roughly a day after mainnet went live. The structural facts here (the stack, the issuer, the partners, the restrictions) are confirmed by Robinhood’s own materials and launch-day reporting. The adoption numbers are not: mainnet TVL, transaction counts, and active addresses are barely a day old, and several figures circulating on crypto Twitter have not been confirmed on-chain. Treat the architecture as settled and the traction as a snapshot of an ecosystem that is hours old.

What Actually Launched

Robinhood Chain is a Layer 2 built on Arbitrum’s Orbit stack (the same Nitro-based technology behind dozens of app-chains), settling to Ethereum and using Ethereum blobs for data availability. Gas is paid in ETH; there is no native chain token, and Robinhood has not announced one. Mainnet chain ID is 4663, testnet is 46630. Standard Solidity and Vyper contracts deploy without changes, and the chain supports ERC-4337 account abstraction for gas sponsorship and batched transactions. Sequencing is first-come, first-served. The developer docs and a Blockscout explorer went live with mainnet.

On the technical merits, this is a conservative, sensible design. Robinhood did not try to invent a new virtual machine or a novel consensus mechanism. It took the most battle-tested L2 stack available, wired in the usual institutional plumbing, and shipped. The day-one integration list is genuinely deep:

| Layer | Day-one partners (per launch materials) |

|---|---|

| Infrastructure | Alchemy (primary RPC), Arbitrum, Chainlink oracles, BitGo and Fireblocks custody, LayerZero, QuickNode |

| Trading / DEX | Uniswap (dedicated AMM), Pleiades (prop-trading AMM), Lighter (order-book perps), with 1inch, Rialto, and Arcus as stock-token venues |

| Lending | Morpho, powering Robinhood Earn, with Steakhouse, Ethena, Spark, and Maple as ecosystem partners |

That is a serious roster to assemble for a first-day launch, and it is fair to say most of the crypto-native skepticism is not aimed at the stack. As one widely shared take put it, the chain is “architecturally serious,” and the real gap is trust in the operator rather than doubt about the tech. So the rest of this piece is about the operator, the asset, and the market structure, because that is where the actual questions are.

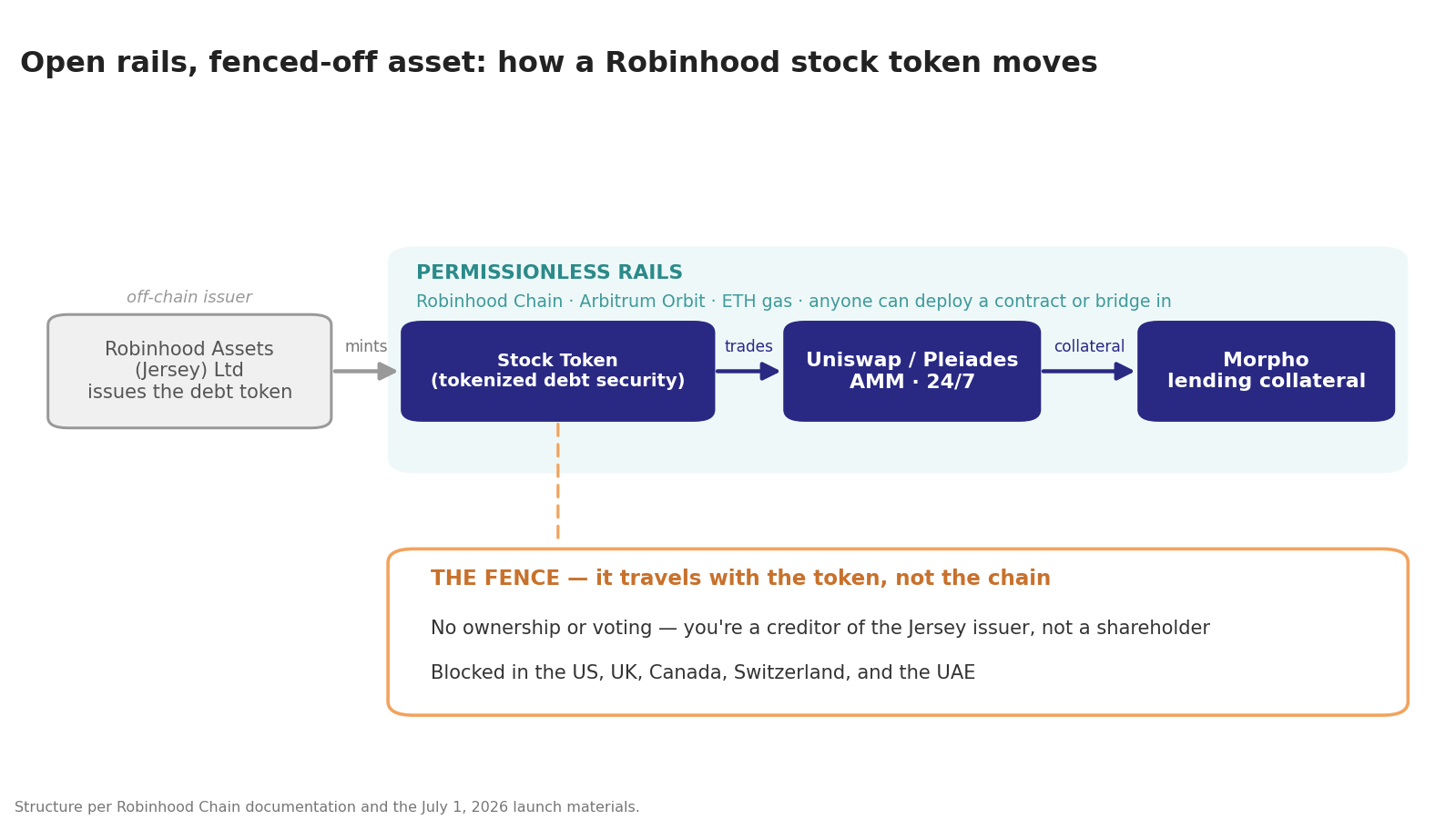

The Flagship Asset Is Not a Stock

Robinhood Chain was built first and foremost for tokenized stocks: round-the-clock exposure to names like Nvidia, Apple, and Alphabet, usable as collateral, lendable, and tradable on-chain. This is the headline feature, and it is the one worth reading the fine print on.

The tokens are not shares. They are tokenized debt securities issued by Robinhood Assets (Jersey) Limited, a subsidiary in the Channel Islands. Holding one gives you price exposure to the underlying stock. It does not give you ownership, voting rights, or a direct claim on the company. What you hold is a liability of a Robinhood entity that tracks the price and is redeemable for cash through authorized participants, with redemption for the actual underlying securities described as a future plan rather than a present feature. If that entity fails, you are a creditor, not a shareholder. This is the same structural model that drew public pushback when earlier tokenized-equity efforts launched, including OpenAI distancing itself from tokens that claimed to represent its equity in 2025.

| Robinhood Stock Token | The actual share | |

|---|---|---|

| What it is | Tokenized debt security | Equity ownership |

| Counterparty | Robinhood Assets (Jersey) Limited | The company itself |

| Ownership / voting | None | Yes |

| Claim if issuer fails | Creditor of the Jersey entity | Shareholder of the company |

| Redemption | Cash via authorized participants (underlying securities “planned”) | Sell on the exchange |

| Who can hold | 120+ countries, not the US, UK, Canada, Switzerland, or UAE | Anyone with a broker |

| Trading | 24/7 on an AMM | Exchange hours, on an order book |

This is also not Robinhood’s first pass at tokenized equities. It switched on more than 200 tokenized US stocks and ETFs for EU and EEA users at an event in Cannes in June 2025; those are now rebranded “Classic Stock Tokens” and stay in the Robinhood Europe app. The new Stock Tokens on Robinhood Chain are the second generation, and the pitch this time is composability: the same tokens can move into DeFi rather than sitting inside one app.

Then there is geography. The tokenized stocks are available in 120-plus countries but explicitly not in the United States, and they are restricted in the UK, Canada, Switzerland, the UAE, and sanctioned jurisdictions. In fairness, the US wall is a regulatory constraint rather than a Robinhood preference; US securities law does not have a clean lane for a retail-traded tokenized debt security wrapping an equity, and Robinhood is not going to pick that fight first. But the effect is the same regardless of the cause. Robinhood’s core audience is American retail, and the flagship product on its new chain is unavailable to most of the people who made Robinhood a household name. Robinhood is rolling out an onchain lending product (Robinhood Earn) for eligible US users, so Americans get a version of the DeFi story, just not the tokenized-equity part that the chain was built around.

Put the two facts together and you get the central tension. The rails are permissionless: anyone can deploy a contract, run a node against the public RPC, or bridge in ETH. The flagship asset is the opposite of permissionless. It is a jurisdictionally gated, ownership-free debt instrument issued by a single company’s offshore subsidiary. The chain is open. The product that justifies the chain is fenced.

For a cleaner way to think about where these tokens sit on the spectrum from “truly on-chain” to “database entry with a wrapper,” the Distributed vs. Represented framework is the useful lens. Robinhood’s stock tokens are mobile and composable, which pushes them toward the Distributed end. But mobility is a separate axis from ownership, and on the ownership axis these are as thin as tokenized RWAs get.

The Liquidity Question Nobody Has Answered

Assume the tokens work exactly as advertised. There is still a market-structure problem, and it is the sharpest of the bearish takes.

The spot venues for the stock tokens on day one are automated market makers: Uniswap’s dedicated public-liquidity AMM and Pleiades, a proprietary AMM for prop trading, with routing through 1inch, Rialto, and Arcus on top. AMMs are excellent for long-tail crypto assets. They are a debatable choice for equities, where price discovery has run on central limit order books for a century and where the reference price updates continuously during market hours. An AMM holding tokenized NVDA has to be arbitraged back to the real quote constantly, and the people doing that arbitrage extract value from the liquidity providers on the other side. Thin books plus a fast-moving external reference price is a recipe for LPs getting picked off, which in turn thins the books further.

Robinhood clearly knows this, because the perps side went a different way: Lighter, the perpetual-futures venue integrated into the wallet, is an order-book DEX, not an AMM. So the chain ships with a CLOB for perps and an AMM model for the tokenized stocks, which are the assets where the order-book argument is strongest. Whether equities can trade well at size on an AMM is the open question, and launching the stock tokens AMM-first is a real bet, not a solved problem. Early liquidity on the stock tokens is exactly the metric to watch over the coming weeks, and it is exactly the metric nobody can cite yet.

The Trust Question

Here is where the buy-button history matters, and not just as rhetoric.

“Permissionless” is doing a lot of work in the marketing. At launch, a single sequencer, run by or on behalf of Robinhood, orders transactions. That is normal for a young Arbitrum Orbit chain; almost every L2 starts centralized and decentralizes its sequencer later, if ever. But it means the entity that once switched off buying during a squeeze is, today, the entity that decides transaction ordering on a chain whose core asset is issued by its own subsidiary. The canonical bridge is trustless and the contracts are open, which is real and worth crediting, though the standard Arbitrum caveat applies: canonical withdrawals back to Ethereum carry the roughly seven-day challenge period, so bridging out is not instant unless you pay a third-party fast bridge to front the liquidity. The sequencer, the issuer, and the app are, for now, the same company.

Two other things feed the skepticism. Robinhood cut about 10% of its workforce in mid-June 2026, weeks before this launch, taking roughly $28 million in restructuring charges as it pushed toward a leaner structure. Management framed the cuts as coming “from a position of business strength,” but the timing reads oddly against the execution demands of standing up a chain, an issuer, a wallet integration, and a lending product at once. And the bootstrap incentive, a confirmed 90 days of covered gas fees for eligible wallet users plus no fees on Lighter perps during the window, is the kind of subsidy that inflates early usage numbers and then expires. None of this is disqualifying. All of it is reason to discount the day-one metrics.

The Metrics, Such As They Are

Because mainnet is hours old, there is very little confirmed on-chain data. What exists is a mix of a testnet benchmark, launch claims, and secondhand figures.

| Signal | Figure | Status |

|---|---|---|

| Testnet activity | ~4M transactions in first week (Feb 2026) | Reported, testnet only |

| Latent distribution | ~28M Robinhood users cited as onramp | Company-scale figure, not chain adoption |

| Gas subsidy | 90 days of covered fees (wallet users) | Confirmed by Robinhood |

| Lighter incentives | ~$11M in LIT for perps liquidity | Ecosystem-project claim |

| Robinhood Earn yield | ~7% APY lending USDG via Morpho, with Lloyd’s of London and RELM insurance on cyber/smart-contract exploits | Confirmed by Robinhood |

| $HOOD reaction | Up ~2% pre-market on the announcement | Reported market move, not a chain metric |

| Mainnet TVL / volume | Not yet meaningfully published | Unknown |

The most important row is the last one. As of writing, there is no widely cited mainnet TVL, transaction count, or active-address figure. Tracking tools are live, and there are mentions of the chain showing up on DEX scanners with “volume heating up,” but nothing you would build a thesis on. The 28-million-user number gets repeated constantly, and it is worth remembering that it measures Robinhood, not the chain. Latent distribution is not adoption until users actually bridge and transact, and most of the people being counted cannot buy the flagship asset.

Two more things the metrics conversation is quietly about. There is no confirmed airdrop or governance token, which has not stopped a familiar wave of point-farming and “mainnet streak” guides from circulating, plus the usual reflexive memecoins launching on any new chain. And while the headline integrations (Uniswap, Lighter, Morpho, Chainlink, BitGo) are genuinely live, “live” and “liquid” are different claims; a deployed AMM with thin depth is still thin. Treat the farming guides as farming guides.

Where It Fits

Strip away the launch noise and Robinhood Chain is a real strategic move by one of the largest retail brokers in the world to own on-chain rails rather than rent them. The obvious comparison is Coinbase’s Base: a large, regulated, US-listed consumer platform standing up an L2 and pointing its user base at it. Base went with a general-purpose OP-stack chain and let the ecosystem decide what to build. Robinhood has chosen an Arbitrum-stack chain with a specific flagship use case, tokenized equities, baked in from day one. Whether a purpose-built chain beats a general-purpose one for this is the bet. And Robinhood is not first to on-chain equities; the debt-security-wrapper approach it uses has been tried before by other issuers, with mixed traction and recurring questions from the underlying companies about tokens they never authorized.

| Robinhood Chain | Coinbase’s Base | |

|---|---|---|

| Stack | Arbitrum Orbit | OP Stack |

| Mainnet | July 2026 | 2023 |

| Design | Purpose-built for tokenized equities | General-purpose |

| Operator | Robinhood (single sequencer, for now) | Coinbase (single sequencer) |

| US access | Flagship stock tokens blocked | Fully available |

The honest framing is the one the more careful threads have already landed on. Bull case: a battle-tested stack, deep day-one integrations, a real 24/7 tokenized-equity unlock for users outside the US, and one of the largest retail distribution funnels in finance. Bear case: the flagship asset is a synthetic debt security that carries counterparty and regulatory risk, is blocked in Robinhood’s home market, and trades on an AMM model that may not suit equities; and the “permissionless” chain is, for now, operated end to end by a company whose most famous moment was restricting trades.

For DeFi builders and users, the practical takeaway is narrower and more useful than the narrative. The chain is open and the tooling is standard, so if you want to deploy or bridge, you can, today. But the thing that makes Robinhood Chain different from the dozen other Orbit chains is the tokenized-stock product, and that product is exactly the part with the most fine print: an offshore issuer, no ownership rights, hard jurisdictional walls, and untested on-chain liquidity. The rails are the easy part. The asset is where the risk lives, and where the next few weeks of real numbers will actually matter.