When Hyperliquid shipped HIP-4 in early May 2026, the headlines went straight to the obvious angle: zero-fee prediction markets, aimed at Polymarket. That framing is real but shallow. The fee war is a sideshow. The interesting question HIP-4 raises is structural, and it has very little to do with what it costs to place a bet.

Polymarket and HIP-4 both let you buy a contract that pays one dollar if an event happens and nothing if it doesn’t. Underneath that shared surface they are built on opposite philosophies about three things: where the market lives, who is allowed to create one, and, most importantly, who decides what actually happened. That third question is where the two designs diverge, and it is the one that will decide whether HIP-4 is a Polymarket killer or a different product that happens to look similar.

This piece reflects the state of HIP-4 as of late May 2026. The outcome-market primitive is new, fees are still set to zero for an initial testing period, and the validator outcome-resolution model has not yet been stress-tested by a contested event. Treat the design described here as the launch version, not the settled one.

What HIP-4 Actually Is

HIP-4 adds a new instrument type to Hyperliquid: the outcome market. These are fully collateralized binary contracts that settle within a fixed range, with two sides, typically labeled Yes and No, that pay out based on a settleFraction of 1 for a Yes resolution and 0 for a No. Buy Yes at 0.60 and you pay 0.60 in the quote asset; if the event resolves true you collect 1.00, and if it resolves false you lose what you put in. The price between 0 and 1 is the market’s implied probability. That is the same payoff structure Polymarket has run for years.

What is different is where it lives. HIP-4 is not a separate application sitting on top of Hyperliquid. It is a primitive baked into HyperCore, the same base layer that already runs the chain’s spot and perpetual markets. Outcome contracts trade on the same on-chain central limit order book (CLOB), settle into the same collateral, and sit in the same account as your perps. Hyperliquid’s own framing is that outcomes add “non-linearity, dated contracts, and an alternative form of derivative trading that does not involve leverage or liquidations.” In plain terms: it is a prediction market that happens to live inside a derivatives exchange, rather than a prediction market that had to build its own everything.

One neat piece of the design is the merged order book. HIP-4 treats an order to buy Yes at price p as identical to an order to sell No at 1 - p, pooling both sides into one book ranked by price-side-time priority. It is a clean way to keep a binary market liquid. It is also not unique. Polymarket’s order book already does the same thing: buying Yes there is matched as selling No, and two complementary buy orders that sum to a dollar mint a fresh set of shares. Both venues landed on the same insight, that a binary market should not split its liquidity across two separate books. So the merged book is a point of convergence, not a Hyperliquid advantage, which is worth stating plainly because the launch coverage tended to sell it as an edge.

HIP-4 sits next to HIP-3, the builder-deployed perpetuals framework Hyperliquid launched in October 2025, which already let outside teams stand up their own perp markets against a staked bond. HIP-4 is the same idea pointed at events instead of price feeds. The first markets, recurring daily Bitcoin price binaries surfaced through builders like Outcome (styled Outcomexyz) and the Stratium frontend, went live on launch day. In late May 2026 Hyperliquid extended the model past crypto into macro: markets on US inflation prints and Federal Reserve decisions, the exact territory Polymarket and Kalshi have built their brands on.

What Polymarket Actually Is

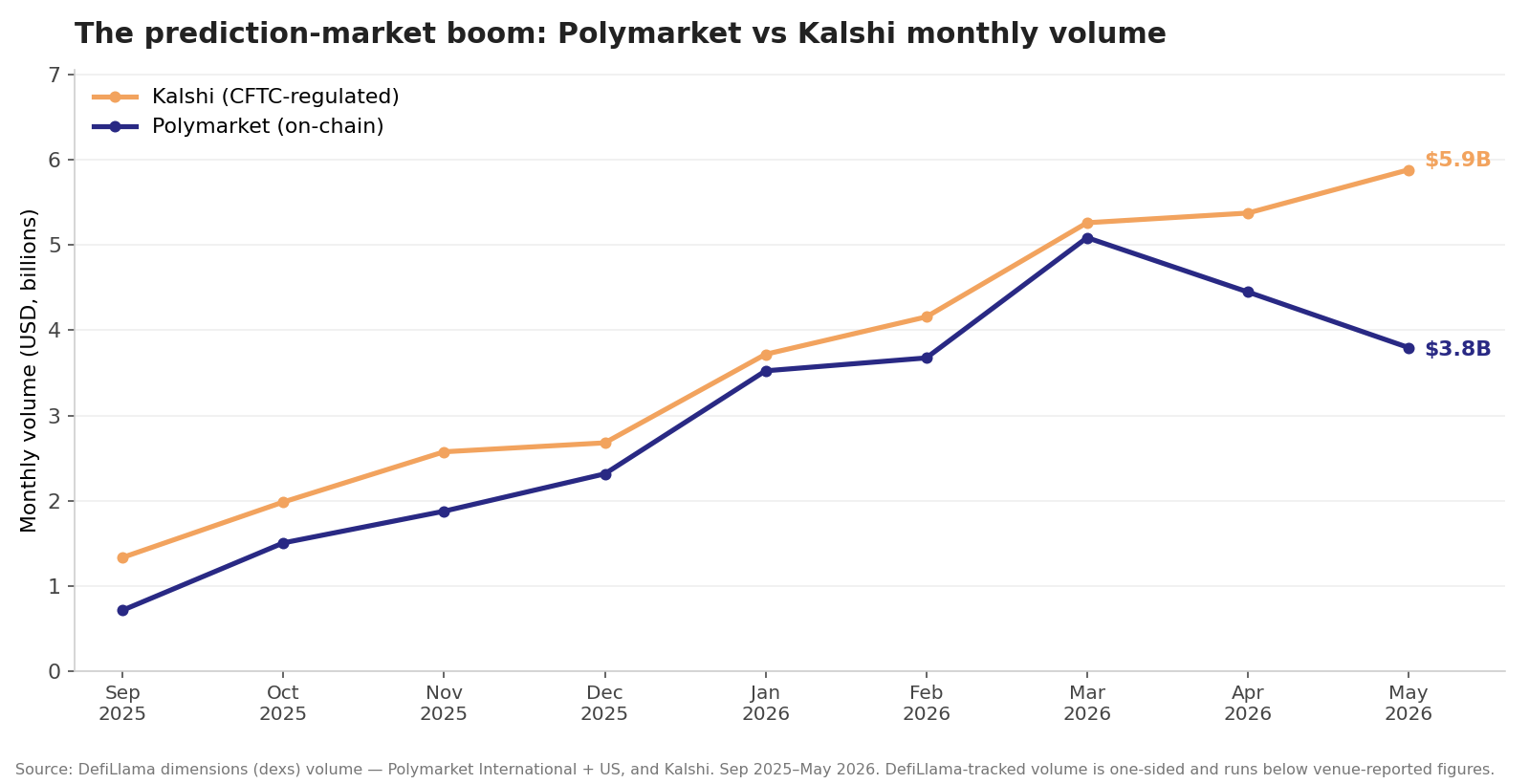

Polymarket is the incumbent, and it is not a small one. By DefiLlama’s count its monthly volume climbed roughly sevenfold across late 2025 and into 2026, peaking near $5 billion in March before easing back. Polymarket’s own headline numbers run about double that, the difference coming down to whether you count one side of each trade or both, but even the conservative read is real scale. It is the largest on-chain prediction market to date, though the CFTC-regulated Kalshi has matched and lately outrun it on the same measure. The category HIP-4 is wading into is booming across the board, well beyond any single venue.

Architecturally it is an application, not a chain feature. Polymarket runs on Polygon. Each market is a set of Gnosis Conditional Tokens, the outcome shares that become redeemable once a result is known, and everything settles in USDC. Order matching happens off-chain through a central limit order book, with settlement on-chain, so the user experience is gasless and the contracts hold the funds.

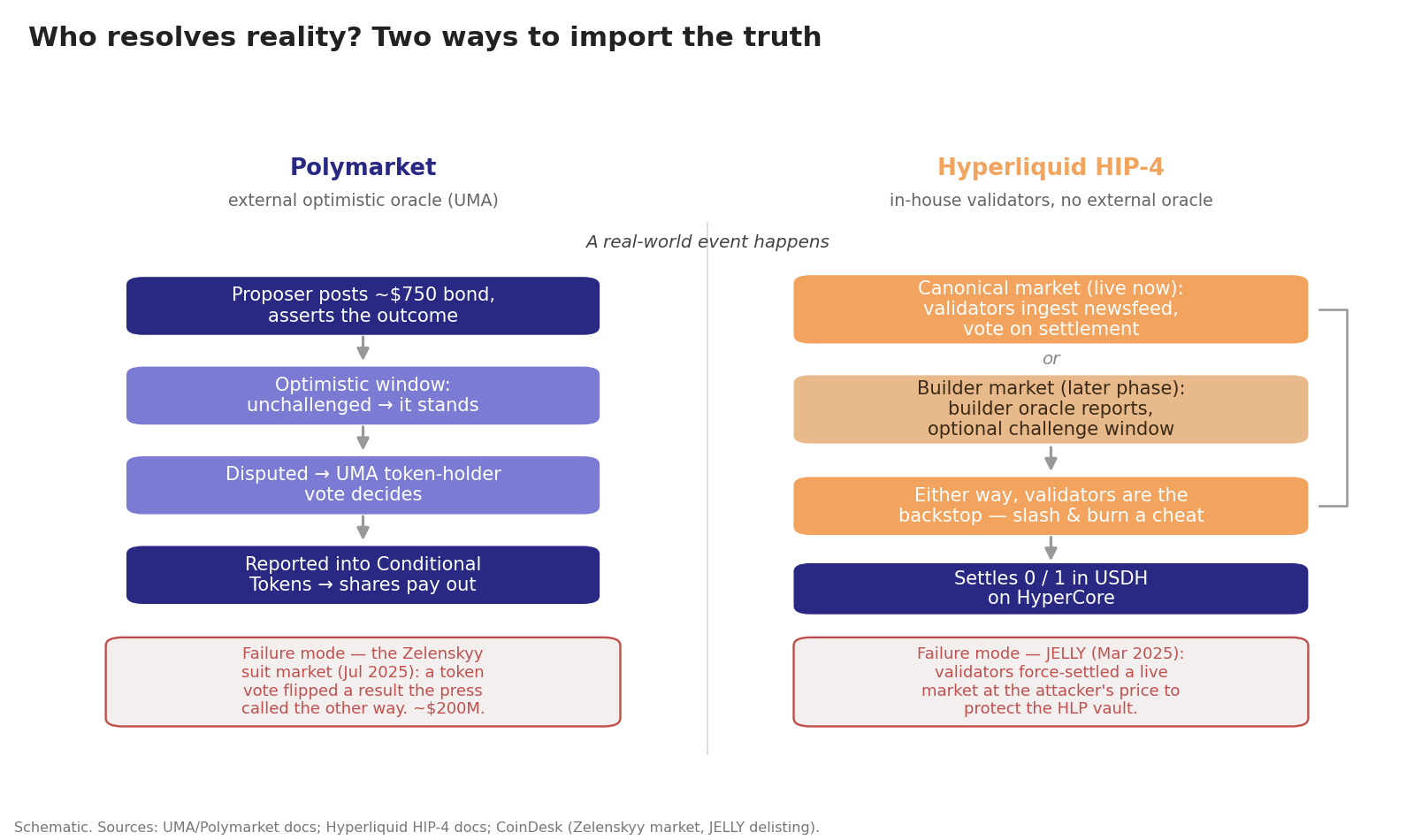

The part that matters for this comparison is resolution. Polymarket does not decide outcomes itself. It outsources truth to UMA’s optimistic oracle, which resolves roughly 78% of its markets. The mechanism is economic: a proposer posts a bond of around $750 USDC asserting an outcome, and if nobody disputes within the challenge window, that answer stands and the proposer earns a small reward. If someone disputes, they post their own bond, and the question escalates to a vote of UMA token holders who are paid to converge on the truth. The security of every Polymarket resolution rests on that external, token-weighted dispute market.

That separation is deliberate. Polymarket is a venue; UMA is the referee; the two are different systems run by different people. It is the same modular pattern we walked through in the Polymarket key-compromise post, where the audited resolution contracts held fine even as a backend wallet got drained. The resolution layer is a distinct, swappable component.

Where They Actually Differ

The resolution layer

This is the real fight, so it goes first.

Polymarket pushes resolution out to an external, permissionless economic game. Anyone can propose, anyone can dispute, and disputes are settled by a vote weighted by UMA token holdings, with participants bonded and rewarded for landing on the answer the majority converges on. The trust assumption is that UMA’s economic security is large enough that corrupting a resolution costs more than it pays. The weakness is latency, ambiguity, and capture. The sharpest illustration is the July 2025 market on whether Zelenskyy wore a suit at the NATO summit, with around $200 million riding on it. Mainstream outlets including the BBC and The New York Times called the outfit a suit, UMA’s oracle initially resolved the market Yes, and then a token-holder challenge flipped it to No. Critics argued the voters were following the perceived majority and the largest holders rather than the plain facts. That is the failure mode of an open economic oracle: it is only as honest as the incentives of whoever holds the most voting weight, and it can be slow and ugly getting there.

HIP-4 brings the referee in-house, but what “in-house” means depends on the market. For the canonical markets Hyperliquid resolves itself, the daily Bitcoin binaries at launch and the macro markets that followed in late May 2026, the validator set, currently 24 nodes and expanding to 27, ingests outside information through newsfeed software and votes on settlement. A later permissionless phase will let outside builders deploy their own markets, where the builder runs an authorized oracle updater that reports the result, with an optional challenge window for disputes and the validator set standing behind it as the slashing backstop if the builder cheats. Either way there is no external oracle protocol. Resolution comes either from the validators who produce the chain’s blocks or from a single bonded reporter they can punish. It is a closed loop, and the entity calling the truth is either the chain operator or one deployer standing on a deposit.

This is not hypothetical, and that is the part worth sitting with. In March 2025, long before HIP-4 existed, the same validator set reached into a live market and changed the outcome. A trader engineered a short squeeze on the JELLY perpetual and left Hyperliquid’s HLP vault facing a roughly $13.5 million loss. Validators voted within minutes to delist the contract and force-settle every position at $0.0095, the attacker’s entry price, rather than the roughly $0.50 the market was actually trading at. Users were later made whole by the Hyper Foundation. Critics called it a “validator put”: when the protocol’s own money is on the line, the validators will overrule the market. More than half the validating stake sat with five Foundation nodes at the time. That is the trust question for HIP-4 in concrete form. The body that resolves your CPI bet has already demonstrated it will override a settlement price when its own vault is exposed.

Each approach trades away something the other keeps. Hyperliquid’s closed loop is faster and removes the external oracle as a separately governed component. “No external oracle” is doing some marketing work, though, because the validators still ingest the outside world through newsfeed software. The dependency on external data does not vanish; it just moves inside the validator set instead of living in a separate protocol. The deeper point is the shape of the trusted group. A validator set of two dozen voting on what the CPI printed, or a lone builder reporting it, is a small and named set of resolvers, and a canonical market offers no external court of appeal, where UMA at least lets a disputant post a bond and force the question to a wider vote. Polymarket’s referee is large and diffuse, but it is not capture-proof either, as the Zelenskyy market showed. The real choice is between two failure modes: Polymarket’s referee is slow and swayable by big token holders, while Hyperliquid’s is fast and is the same party that runs the exchange and the vault. Pick your poison.

If you only remember one distinction between these two products, make it this one.

Who gets to create a market

Both platforms are more permissioned than the marketing suggests, in opposite ways.

On Polymarket, creating a market is cheap in capital, around a $750 bond to propose a resolution, but the menu of markets is curated by Polymarket itself. You are mostly a price-taker on which questions exist.

On HIP-4, the markets live at launch are canonical ones the validators choose and resolve, so for now the gate is validator selection, not open access. Permissionless deployment is slated for a later phase, and there a builder who wants to stand up their own outcome market posts a stake reported at around 1,000,000 HYPE, slashable and burned if they manipulate the oracle, push invalid state, or let the market go dark. Hyperliquid has not published a final contract spec, so treat that as the widely cited number rather than a locked parameter. At roughly $65 a token in late May 2026 it works out near $65 million, though it behaves as a reusable deployer slot rather than a per-market fee: once a market resolves, the slot can be recycled for the next event. Even as a one-time cost to become a deployer, a bond that size is a barrier only a handful of well-capitalized teams can clear. Either way the set of entities that can mint a Hyperliquid outcome market is small. Polymarket gates by editorial control; HIP-4 gates by validator choice now and by capital later.

Liquidity and the order book

Both run central limit order books with the same merged Yes/No design, so the headline mechanics match. The difference that matters is where the matching happens. Polymarket matches orders off-chain and settles them on-chain on Polygon, a hybrid that keeps the experience fast and gasless. HIP-4 matches on-chain inside HyperCore, in the same engine and the same margin account as a trader’s perps, so someone can hold a Fed-decision position next to a leveraged BTC long against one pool of collateral. That cross-margin proximity is HIP-4’s structural edge, not the book design. Against it, Polymarket has the one thing that actually makes a prediction market work: liquidity. Years of volume, a deep base of traders, and the name people reach for during an election or a breaking story. A matching engine does not beat a liquid book on day one, and HIP-4 is starting close to scratch. Its flagship daily Bitcoin binary drew around 4,000 traders on launch day and roughly 0.7% of global prediction-market volume, which is real traction for a brand-new instrument and a rounding error next to the billions a month Polymarket and Kalshi each clear.

Fees and the unit of account

The fee story is the one everyone leads with and it is the least durable. HIP-4 charges no protocol fee to open a position during its initial testing window, though a builder fee can still apply, and builders can take a share of up to 50% on top of Hyperliquid’s base fees. Polymarket has historically run near-zero trading fees of its own. Both can change at any time. Treating “zero fees” as HIP-4’s moat misreads which parts of this are structural and which are promotional.

The settlement currency is a quieter but stickier difference. Polymarket settles in USDC, full stop. HIP-4 markets, at launch, settle in USDH, Hyperliquid’s own stablecoin, so a trader funding a position first has to swap USDC into USDH on the spot market. The awkward part is timing. USDH is on its way out: after Coinbase became Hyperliquid’s official USDC treasury deployer in May 2026, the chain began migrating quoting and settlement toward USDC and started winding USDH down. So HIP-4 shipped settling in the one stablecoin the ecosystem is actively retiring, with the move to USDC still in flight. It is a transitional wrinkle rather than a deep flaw, but it is a wrinkle Polymarket simply does not have.

Regulation

This is the difference that may matter most outside the protocol design, and it cuts against Hyperliquid.

Polymarket spent 2025 buying its way back into the United States. It acquired the CFTC-licensed exchange and clearinghouse QCEX for $112 million, secured an amended CFTC order allowing intermediated US access through brokers and futures commission merchants, and took an investment of up to $2 billion from Intercontinental Exchange, the owner of the New York Stock Exchange, at an $8 billion valuation. Polymarket is walking, deliberately and expensively, toward being a regulated US venue with institutional plumbing behind it.

HIP-4 is the opposite posture: offshore, permissionless, no KYC, with event resolution performed by a validator set that answers to no regulator. For crypto-price outcomes, nobody much cares. For markets on US inflation, elections, and Fed decisions, that is precisely the territory the CFTC has been most assertive about. The product that wins on decentralization may be the one that struggles most to touch regulated US flow, and the product carrying compliance overhead may be the only one a US institution can legally use. Decentralization and distribution are pulling in different directions here.

The Numbers Worth Anchoring On

| Hyperliquid HIP-4 | Polymarket | |

|---|---|---|

| Launched | May 2, 2026 (testing); macro markets May 26, 2026 | Live since 2020 |

| Architecture | Primitive inside HyperCore; on-chain CLOB matching | App on Polygon (Conditional Tokens); off-chain matching, on-chain settlement |

| Resolution | No external oracle: validators vote on canonical markets; builder-run oracle + validator slashing on builder markets | UMA optimistic oracle (~78% of markets) |

| Order book | Merged Yes/No book | Merged Yes/No book |

| Cost to create a market | Validator-curated at launch; permissionless builder path later at ~1,000,000 HYPE reported (~$65M; reusable slot) | Curated by Polymarket; ~$750 bond to propose a resolution |

| Settlement asset | USDH at launch (swap USDC→USDH); migrating to USDC | USDC |

| Fees | No protocol open fee in testing; builder fee up to 50% share | Historically near-zero trading fees |

| Validator set | 24 nodes, expanding to 27; majority of early stake in 5 Foundation nodes | n/a (resolution outsourced to UMA) |

| Precedent for intervention | JELLY perp force-settled by validator vote (Mar 2025) | $200M Zelenskyy market flipped on UMA dispute (Jul 2025) |

| Regulatory posture | Offshore, permissionless, no KYC | CFTC-designated US relaunch; ICE-backed |

| Scale | ~0.7% of global prediction-market volume on day one | ~$5B/mo peak on DefiLlama (Mar 2026); ~2× that by venue-reported figures |

(HYPE was trading around $65 in late May 2026, near an all-time high; the deploy stake is reported rather than confirmed in a final spec, and its dollar value moves with the token.)

The Uncomfortable Questions

Can a small set of resolvers be trusted to call macro reality? Slashing punishes provable manipulation, but a lot of resolving an event is judgment, not arithmetic. A delayed or revised government statistic, an ambiguous Fed statement, an event that half-happens. The validator set began under heavy Hyper Foundation control and is still decentralizing, which makes the “who exactly is voting” question fair to keep asking. And on a builder-deployed market the first call comes from one bonded reporter, not a vote at all. UMA’s open dispute market handles the same ambiguity slowly and contentiously, as the Zelenskyy market showed; HIP-4 handles it quickly and with fewer hands on the result. Neither is obviously safe.

Can HIP-4 bootstrap real liquidity? Its structural edge is the single margin account, trading event contracts and perps against one collateral pool, which is genuinely useful for a crypto trader hedging macro. But liquidity follows traders, not features. Polymarket’s depth came from being where the action was during elections and major news, and 0.7% of global volume on day one is a start, not a moat. HIP-4 has to convert Hyperliquid’s existing perp traders into prediction-market traders, and that conversion is not automatic.

Does HIP-4’s decentralization box it out of the market that matters? The most lucrative event markets, US politics and macro, are also the most regulated. Polymarket is paying a fortune to be allowed to serve them onshore. A permissionless, validator-resolved venue may own the offshore long tail while being structurally locked out of the regulated core.

What is HIP-4 actually competing for? The single-account pitch, trade perps and event contracts on the same collateral, is real and aimed at existing Hyperliquid users hedging macro alongside crypto. That may be a different and smaller game than Polymarket’s mainstream “bet on the news” audience. Same payoff structure, different customer.

The Takeaway

HIP-4 is a sharp piece of design. Folding outcome markets into the exchange primitive, sharing one margin account with perps, and resolving in-house with no external oracle is a cleaner architecture than bolting a prediction market onto a general-purpose chain and renting an oracle to settle it. On engineering, Hyperliquid has a case.

But the thing it optimized away is the thing Polymarket treats as a feature. Polymarket keeps the referee separate from the venue and pays for that separation in latency and the occasional ugly dispute, the kind that put $200 million on whether a jacket counted as a suit. Hyperliquid collapses the referee into the chain itself, a validator vote for canonical markets and a single bonded builder for the rest, and buys speed and self-sufficiency at the cost of concentrating who gets to call the truth. Neither is the obviously correct call. It is a fork in how you build a market that has to import facts from the outside world.

The fee war will be noise within a year. The resolution question will still be there. Whoever you trust to tell you what the CPI printed, an open economic dispute market or the validators running the chain you are trading on, is the entire bet. Everything else is plumbing.