I’ve been advocating for DeFi for a long enough time and tested by myself most of the products presented at DeFiprime. But now I think it’s the right time for skin in the game experiment.

The idea is simple I had put $100 worth into various DeFi lending products, and going to track results over the year. The goal is to increase my wealth in dollar values, and proof that DeFi is the thing and could be sustainable. How good could DeFi products be, comparing to a regular savings account? What would happen if one of the project’s smart contracts get hacked? How DeFi lending rates changes over time? Let’s figure this out.

For this experiment, I will skip fiat on-ramp hassle, and deposit 3.02 ETH(~$515 to cover gas fees) directly to the wallet 0xa51cE0796d32e3cc932C9a9e01663F68f71D9CBf, and then I’ll exchange ETH to the stablecoins I needed at one of the DEXes.

Compound, Nuo, dYdX, and Fulcrum can be described as autonomous money markets. These platforms enable users to earn interest and borrow digital assets without relying on a counterparty. Digital exchanges commonly offer similar features but either the exchange or users need to provide liquidity to allow traders to borrow assets and trade on margin and users need traders to borrow funds to maintain an attractive interest rate. Idle Finance differs in that it aggregates lending protocols to allow users to automatically shift funds between protocols depending on which platform offers the best interest rate at the time.

DeFi products chosen in no particular order, and I don’t take any extra precautions against smart contract hacks such as Nexus Mutual insurance. The reason for choosing USDC over DAI for NUO is that I don’t want to put all of my eggs in one basket, also interesting to check a long time difference between DAI and USDC.

This experiment will help demonstrate the differences between lending protocols in DeFi and contribute to the development of a historical record that can be used for comparing investment opportunities in DeFi.

Experiment conditions

- Starting date: September 1, 2019.

- Experiment duration: 12 months.

- $100 DAI deposited to Compound, txid

- $100 USDC deposited to Nuo, txid

- $100 DAI deposited to Fulcrum, txid

- $100 DAI deposited to dYdX, txid

- $100 DAI deposited to Idle, txid

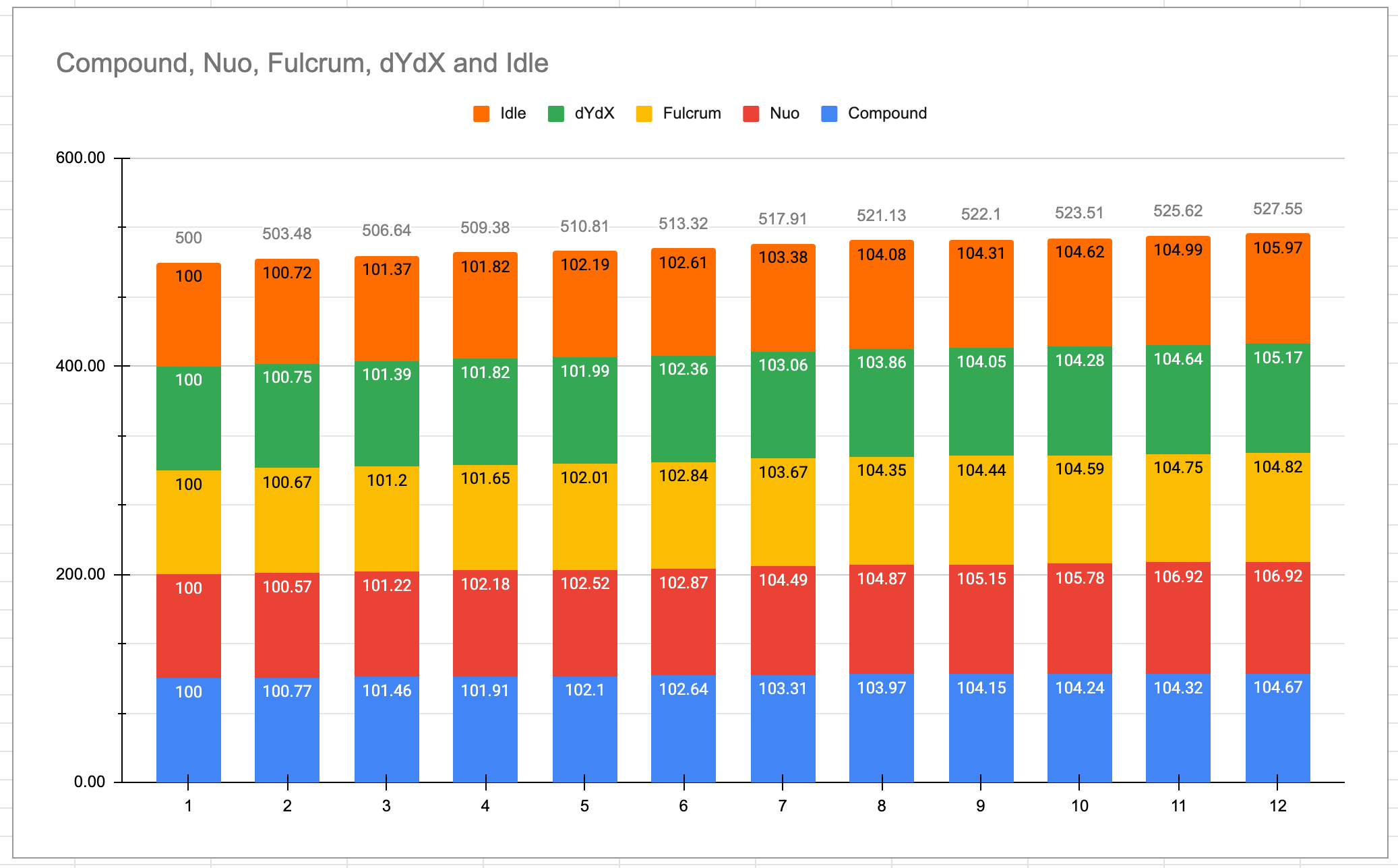

Results Chart

| Product | 09/01 | 10/01 | 11/01 | 12/01 | 01/01² | 02/01 | 03/01 | 04/01 | 05/01 | 06/01 | 07/01 | 08/01 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Compound | 100 DAI | 100.77 +0.77 | 101.46 +0.69 | 101.91 +0.45 | 102.10 +0.19 | 102.64 +0.54 | 103.31 +0.67 | 103.97 +0.66 | 104.15 +0.18 | 104.24 +0.09 | 104.32 +0.08 +$0.36 worth of COMP | 104.67 +0.35 +$0.52 worth of COMP |

| Nuo¹ | 100 USDC | 100.57 +0.57 | 101.22 +0.65 | 102.18 +0.96 | 102.52 +0.34 | 102.87 +0.35 | 104.49 +1.62 | 104.87 +0.38 | 105.15 +0.28 | 105.78 +0.63 | 106.92 +1.14 | - |

| Fulcrum | 100 DAI | 100.67 +0.67 | 101.20 +0.53 | 101.65 +0.45 | 102.01 +0.36 | 102.84 +0.83 | 103.67 +0.83 | 104.35 +0.68 | 104.44 +0.09 | 104.59 +0.15 | 104.75 +0.16 | 104.82 +0.07 |

| dYdX | 100 DAI | 100.75 +0.75 | 101.39 +0.64 | 101.82 +0.43 | 101.99 +0.17 | 102.36 +0.37 | 103.06 +0.70 | 103.86 +0.80 | 104.05 +0.19 | 104.28 +0.23 | 104.64 +0.36 | 105.17 +0.53 |

| Idle | 100 DAI | 100.72 +0.72 | 101.37 +0.65 | 101.82 +0.45 | 102.19 +0.37 | 102.61 +0.42 | 103.38² +0.77 | 104.08 +0.70 | 104.31 +0.23 | 104.62³ +0.31 | 104.99 +0.37 | 105.97 +0.98 |

- ¹ Deposit in USDC

- ² Legacy DAI converted into multicollateral DAI

- ³ Migration to Idle V3

You can track live experiment stats here: 0xa51cE0796d32e3cc932C9a9e01663F68f71D9CBf

I’m going to update the results in this table each 1st day of the month, and provide screenshots from lending platforms dashboards to proof data.

Update: October, 1, 2019

No surprises so far, no one was hacked, and money doesn’t got disappear this month. DeFi rates have been in a range of 8-10% in September.

Update: November, 1, 2019

DeFi rates have been in a range of 6-7% in October.

Update: December, 1, 2019

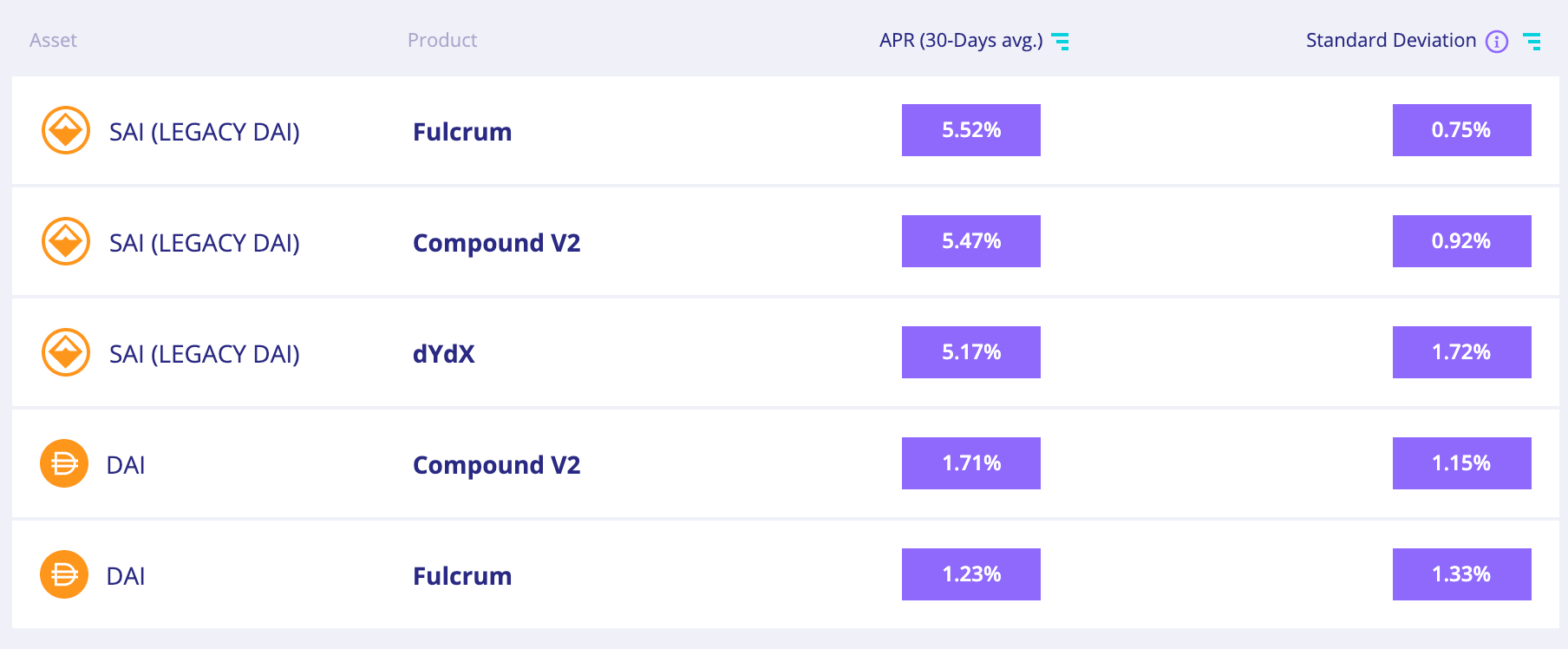

November was a fascinating month for DeFi enthusiasts, due to MakerDAO’s transition to multi collateral DAI, and conversion from SAI (Legacy single collateral DAI) to a new DAI. Most of the DeFi lending protocols published their own transitions plans. Moreover, Fulcrum and Compound already launched markets for the new DAI. I’m not going to migrate from SAI to DAI just yet, because APR for SAI is better at the moment:

Interesting that Fulcrum offers SAI to DAI migration right from UI:

Update: January, 1, 2020

Lending APR for DAI has flipped SAI rates, so this month I’ll convert SAI to DAI on Fulcrum and Compound. The dYdX already had converted SAI to DAI in a centralized manner, so no extra steps from the user required.

Update: February, 1, 2020

Since data verifiable on-chain I decided to get rid of the “proof” screenshots on this page and simplify reporting in a table above. Worth mentioning that the only Idle is still in SAI at the moment, while others are already in DAI. Speaking of APR, looks like we are on a track to 10% APR by the end of this spring.

Update: March, 1, 2020

Finally, someone got hacked! Fulcrum suffered from two attacks in February, happily, DAI lenders funds wasn’t affected. But need to mention that after two hacks, users rushed to withdraw funds from Fulcrum pools, and thus bank run happens. If you want to get out of Fulcrum DAI lending pool, you need to look for available liquidity. Since I’m not going to pull off the money until the end of an experiment, I’ll keep it in Fulcrum.

Update: April, 1, 2020

What a turn of events during March 2020! Crypto Industry’s Black Thursday and issues with MakerDAO effectively wiped off APR from double-digit numbers down to 2-3% range. On a bright side, liquidity is back on Fulcrum and I can withdraw DAI any time if I want to.

Update: May, 1, 2020

9 months of our experiment are already behind!

Update: June, 1, 2020

May was relatively calm for the DeFi lending space, despite much-awaited Bitcoin halving. Lending APR for stablecoins is in the 1-3% range. Combined with high gas fees on Ethereum it makes it economically meaningless to engage with lending protocols if your TX less than $100 in value.

Update: July, 1, 2020

What is interesting this month is how COMP farming affected our experiment data. At the moment of writing roughly 4x of lenders monthly earning is a COMP value. 0.00174725 COMP earned this month, 1 COMP = $214.14. Not going to sell till the end of experiment, so my final numbers are subject to change. Mid July Update: somehow I missed that minimal reserve size for NUO is now set at 3ETH, with 0% APR for anything less.

Last update August, 1, 2020.

It’s a final update of our experiment! We got a lot of interesting data on lending protocol performance in the last 12 months. I guess the most crucial observation is that DeFi is here to stay. Noone exit scammed me, nor critical smart contract collapse happens. And I was able to withdraw my money back successfully.

Key takeaways:

- DeFi lending is not a passive income. You have to follow the space carefully. Protocol and token updates, migrations, and so on is a common thing.

- 12 Months ago, $100 worth was a decent amount to play with experimental technology. Today, I wouldn’t bother with anything less than $1000 because of gas costs to get in and get out of protocol. Small deposits don’t make sense economically anymore.

- It’s not for retail users in any way or meaning as it is now. DeFi lending itself does not solve problems of the mythical unbanked. UX is complicated, and fiat onboarding/offboarding and TX costs for getting in and getting out of the protocols is sky-high.

- APR fluctuates a lot, and recently added incentives in the form of governance tokens distribution affected earnings as well.

Now it’s charts time.

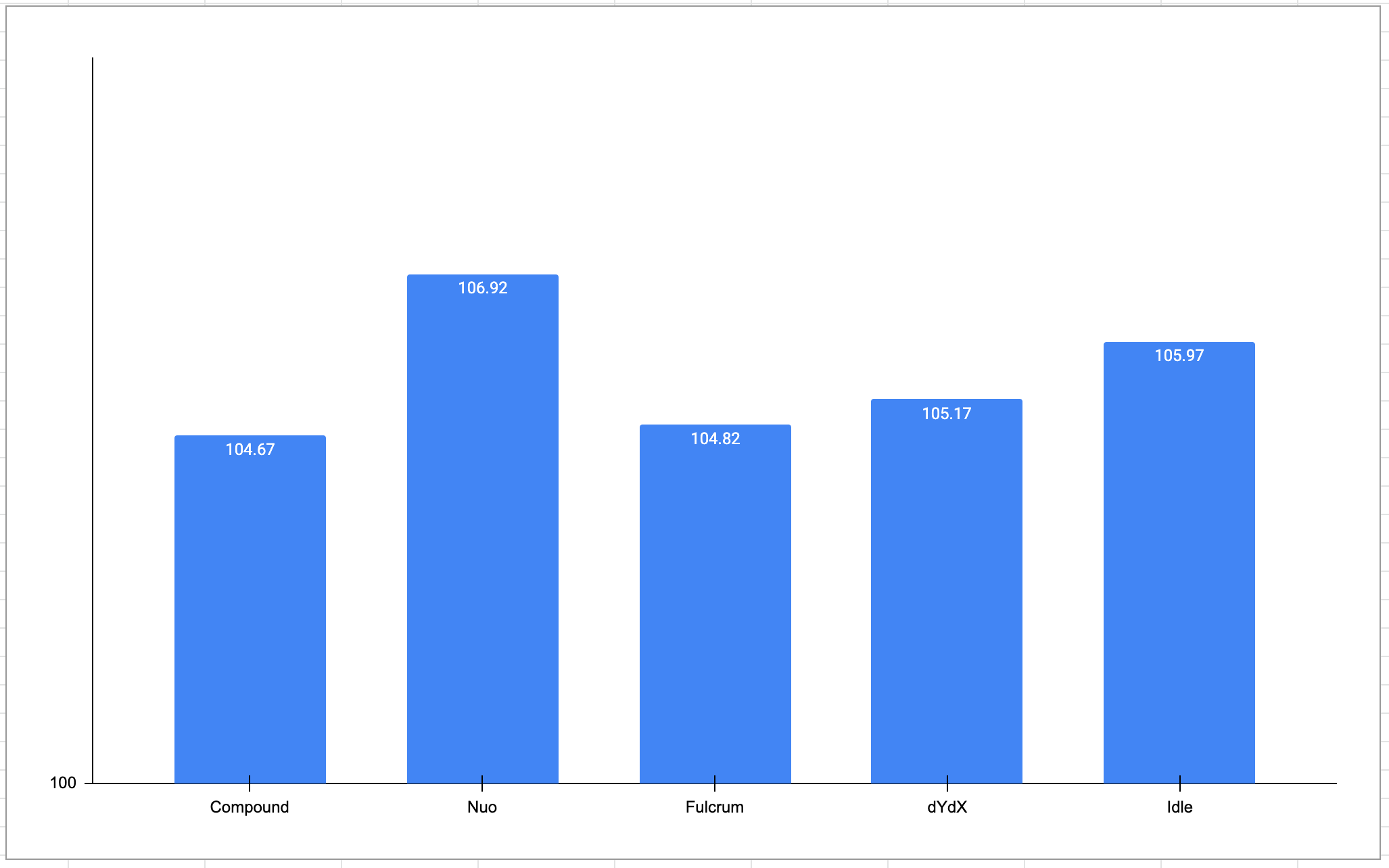

12 months profits breakdown:

Final profits:

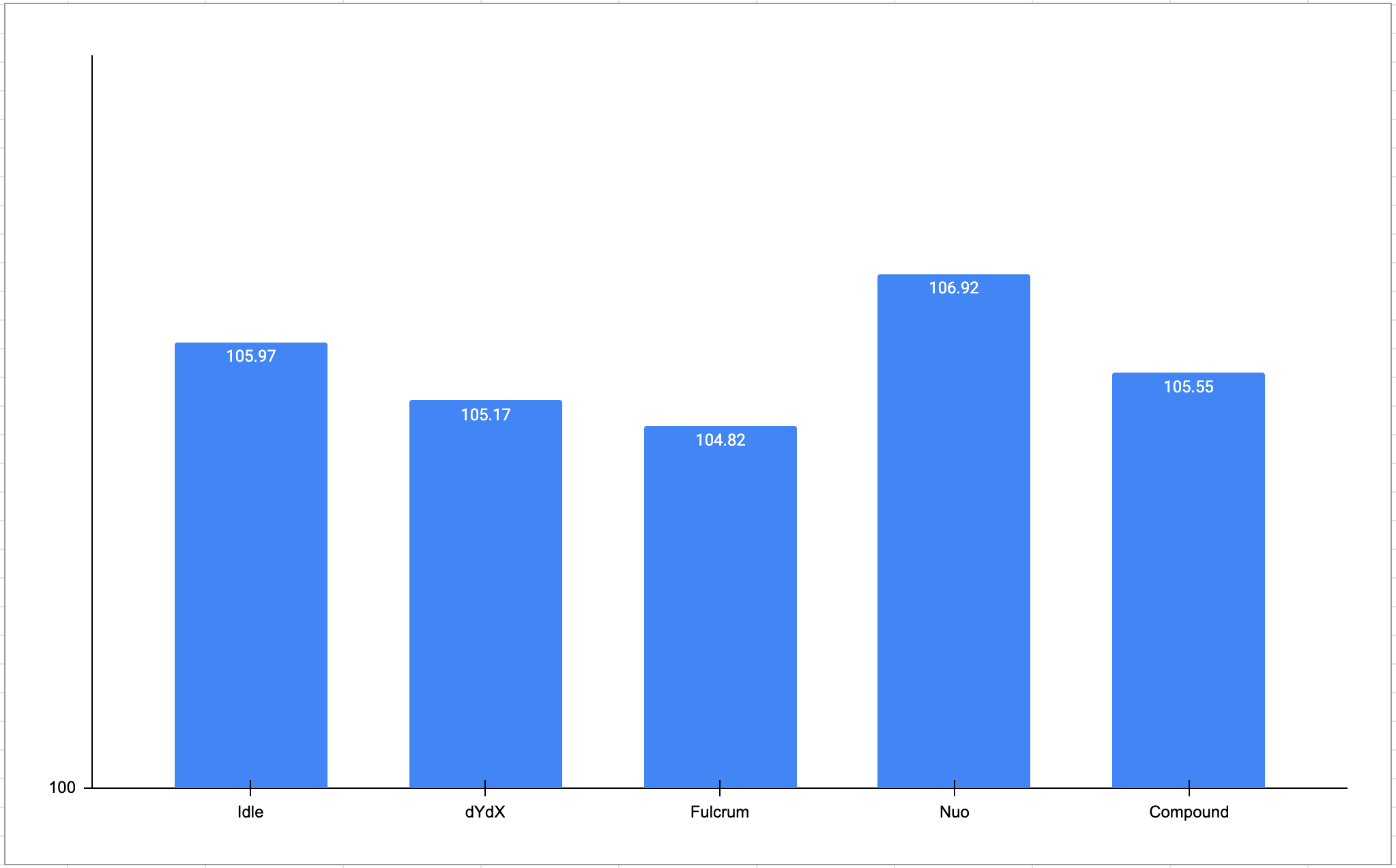

What if we include profits from COMP distribution into Compound results?

And lastly, ouch these gas prices. After 12 months gas cost has eaten all the profits:

As final words I think it’s good to mention how ETH cost had changed: 3.02 ETH worth of ~$515 we had at the start of the experiment now would be $1078.

Do you like this experiment and want to support our work and future researches? Now you can use Gitcoin Grants for that!