On-chain forex looks like a category that should be working by now. Hyperliquid trades twenty-four hours a day, Trade[XYZ] relays institutional LP quotes through a HIP-3 deployment, and Ostium offers 200x leverage on nine major pairs from an Arbitrum vault. The pieces are in place. The volume is not. Combined daily forex volume across the meaningful on-chain venues sits in the $60–110 million range against an interbank market that clears roughly $7.5 trillion a day. That ratio is not a launch curve. It is a structural ceiling, and the reason has very little to do with venue design.

What actually clears on Hyperliquid, Trade[XYZ], and Ostium under the label of “forex” is a USDC perpetual on a price feed. A trader posts USDC, takes directional exposure on EUR/USD or USD/JPY, and settles profit and loss in USDC. Retail FX at offshore brokers is mostly the same shape, since CFDs settle in the funded currency rather than in the quoted instrument, so on-chain venues are not offering a structurally inferior product. The honest framing is not “this isn’t real forex.” It is “this is the same speculative product offshore brokers run, with a different trust model, serving an audience that is small inside DeFi and reachable mainly outside it.”

What Is Actually Live

Three venues do real volume in on-chain currency pairs. None of them lead with forex.

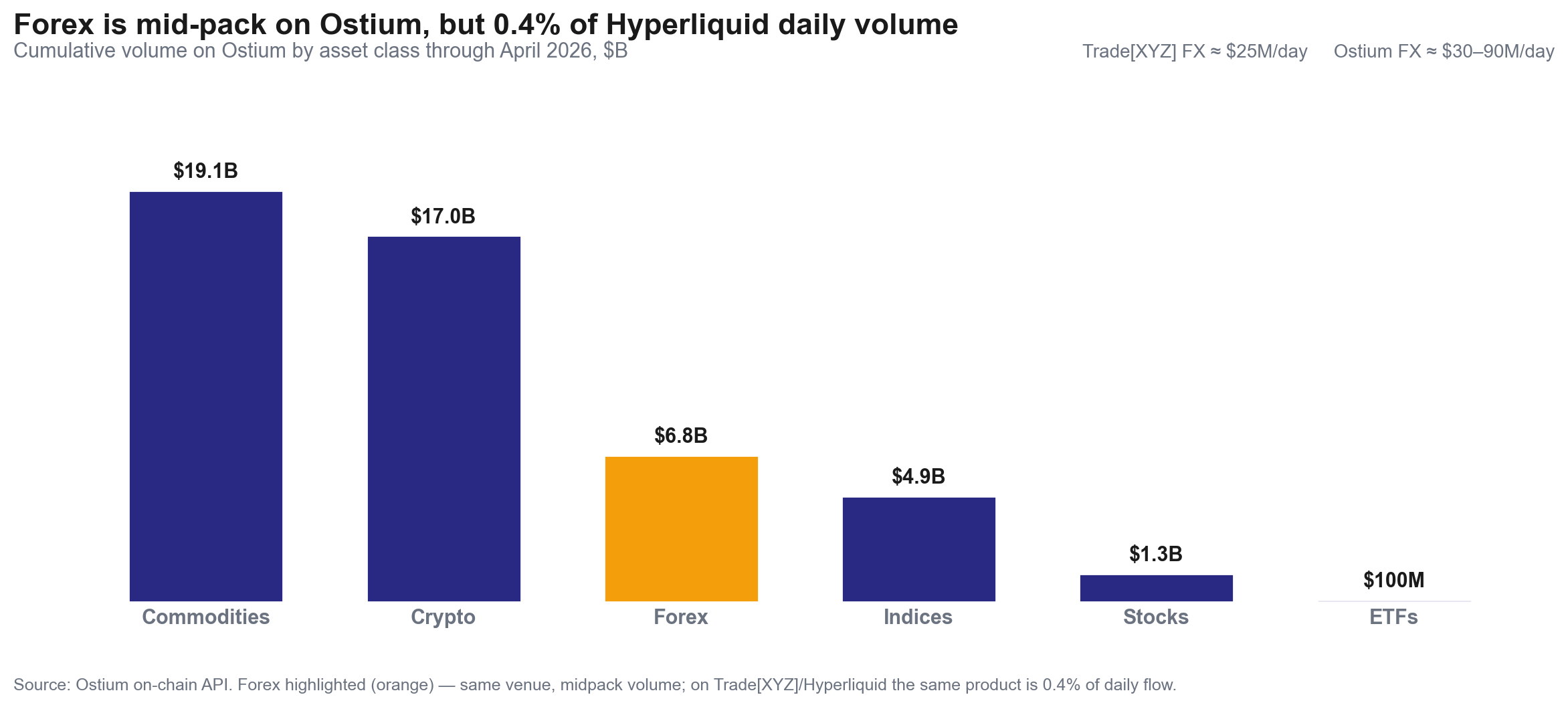

Hyperliquid itself lists zero native forex pairs. Every currency pair on Hyperliquid exists through Trade[XYZ], the dominant HIP-3 deployer, which has standardized two to three active pairs (EUR/USD, USD/JPY, with EUR/JPY less liquid) at around $25 million per day combined. That is roughly 0.4% of Hyperliquid’s daily volume, which tells you exactly how much priority forex gets when the deployer earns 50% of trading fees and has an oil book that peaked at $1.7 billion in a single day. Each new HIP-3 listing slot is better spent on a stock or a commodity than on another currency pair, and the listing economics make that bias durable.

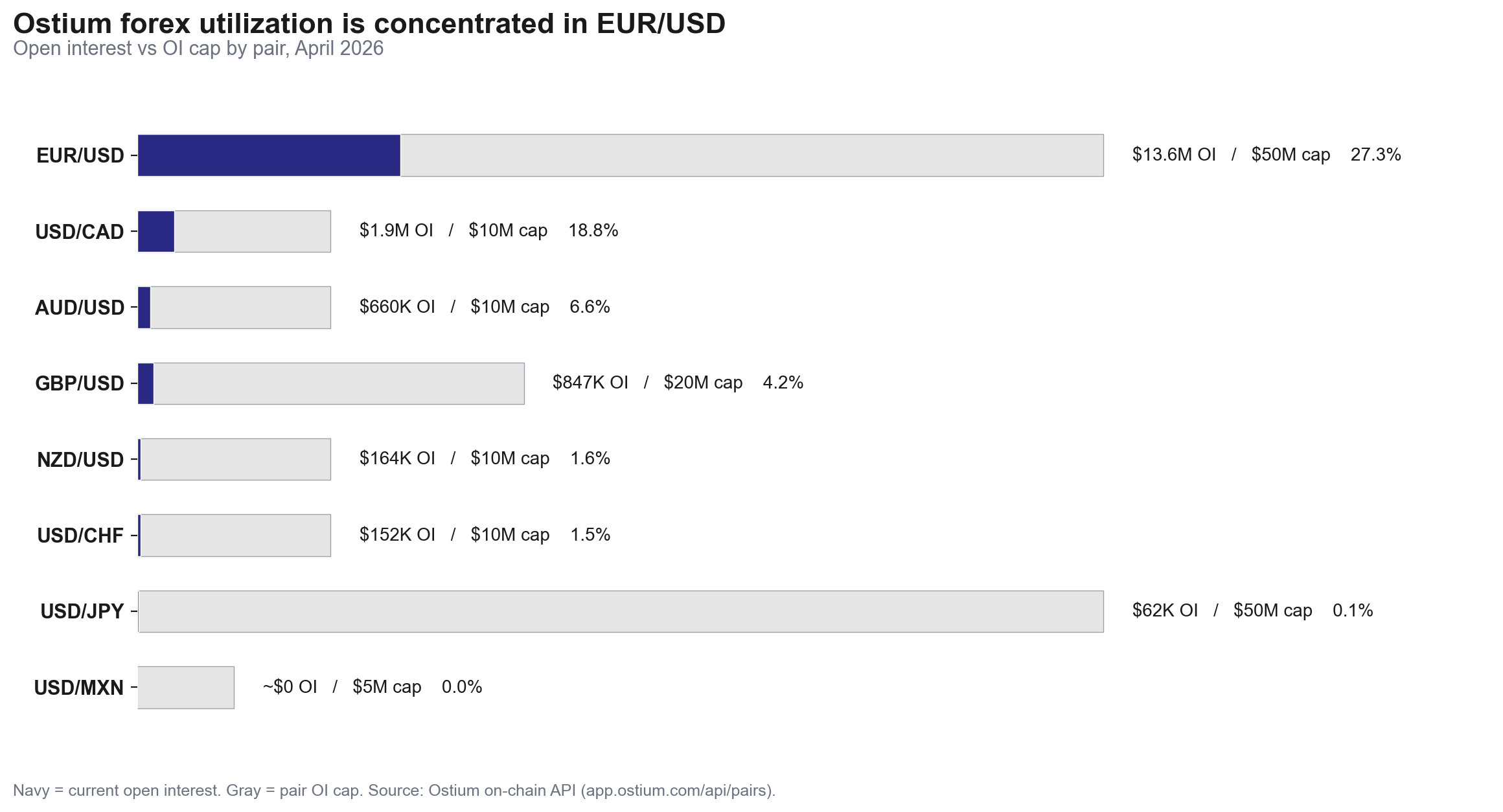

Ostium on Arbitrum is the more developed forex offering by every numerical measure. Nine pairs, $50 million open-interest caps on its top two (EUR/USD and USD/JPY), $10–20 million caps on the rest of the majors, 200x leverage, and roughly $30–90 million in daily forex volume backed by a $53.6 million vault that takes the other side of every trade at the oracle bid/ask. Cumulative forex volume on Ostium is around $6.8 billion since launch, with EUR/USD and USD/JPY accounting for 87% of it. The remaining seven pairs (GBP/USD, AUD/USD, USD/CAD, USD/CHF, NZD/USD, USD/MXN, USD/KRW) carry $150K to $1.9M in standing OI each. The pool architecture is what enables the leverage and the flat fee structure, and it is also what caps the ceiling: dynamic spreads are off, so a $100K trade and a $1M trade face the same execution cost, which is great for users and a balance-sheet problem for the vault if directional flow ever concentrates.

The chart makes the concentration visible: only EUR/USD runs at meaningful utilization against its cap, and USD/JPY has a $50M cap with effectively no standing OI. The seven long-tail pairs are nominally listed but barely traded.

dYdX, Injective, and the rest of the perps field do negligible forex volume. None of them have made it a category priority either.

The structural supply problem sits one layer below any of these venues. Real forex liquidity comes from interbank markets through bilateral relationships with institutional market makers (Citi, Deutsche, XTX, Jump, Virtu) that quote tight on majors because they get paid through prime brokerage relationships, not through exchange fees. Those market makers do not get paid enough on a permissionless DEX with crypto-native users to justify the integration work, and there is no version of HIP-3 economics or vault design that fixes that gap. Trade[XYZ]’s “institutional LP quote relaying” is the workaround, not a solution: it gives users a tighter spread during open sessions and falls back to discovery bounds the rest of the time.

Stocks Work, Forex Doesn’t, and the Difference Is Demand

The cleanest comparison sits one row over in the same venue. Tokenized stocks face the identical primitive issue: a perp on TSLA settled in USDC is not ownership of a Tesla share, has no voting rights, no dividend mechanics, and no path to deliver the underlying. By the “synthetic perp isn’t real exposure” logic, tokenized stocks should be the same dead category as on-chain forex. They aren’t. Trade[XYZ]’s equities book is the most active part of its venue, the S&P 500 perp got an official S&P Dow Jones license in March 2026, and AAPL, TSLA, NVDA, MSFT, and the meme-stock cohort all carry meaningful OI.

The volume picture across venues makes the demand point. On Ostium, forex sits roughly mid-pack at $6.8B cumulative; on Hyperliquid, where commodities and equities pull the user base, forex through Trade[XYZ] is 0.4% of daily flow. Same product, two very different audience responses depending on what else is on offer.

The reason equities work is demand. Crypto-native traders care about earnings catalysts, IPO narratives, and leverage on stocks they already follow on Twitter. TSLA at 20x leverage is a recognizable trade. EUR/USD at 50x is not, because nobody on crypto-Twitter has a view on the euro. The synthetic-perp shape is not the problem; the audience pull is. Forex has the wrong narrative density for the user base, the wrong daily-convexity profile against unlevered crypto, and no memetic hook the way meme stocks have on Trade[XYZ] or oil has on the commodities side. The venue mechanics are identical. The audience response is not.

This is the framing the “on-chain forex” conversation usually misses. The category isn’t broken because the venues built the wrong thing. It’s quiet because the demand-side audience for currency-pair speculation inside DeFi is small, and the demand-side audience for actual non-USD currency holding doesn’t exist on-chain at all.

The Asset-Primitive Gap

The deeper reason on-chain forex stays shallow is that the underlying primitive for real currency exposure does not exist at scale on-chain. This is the part of the story that gets understated when the conversation centers on venue design.

The relevant picture, as of April 2026 (against an aggregate stablecoin float we covered in stablecoins past $320 billion):

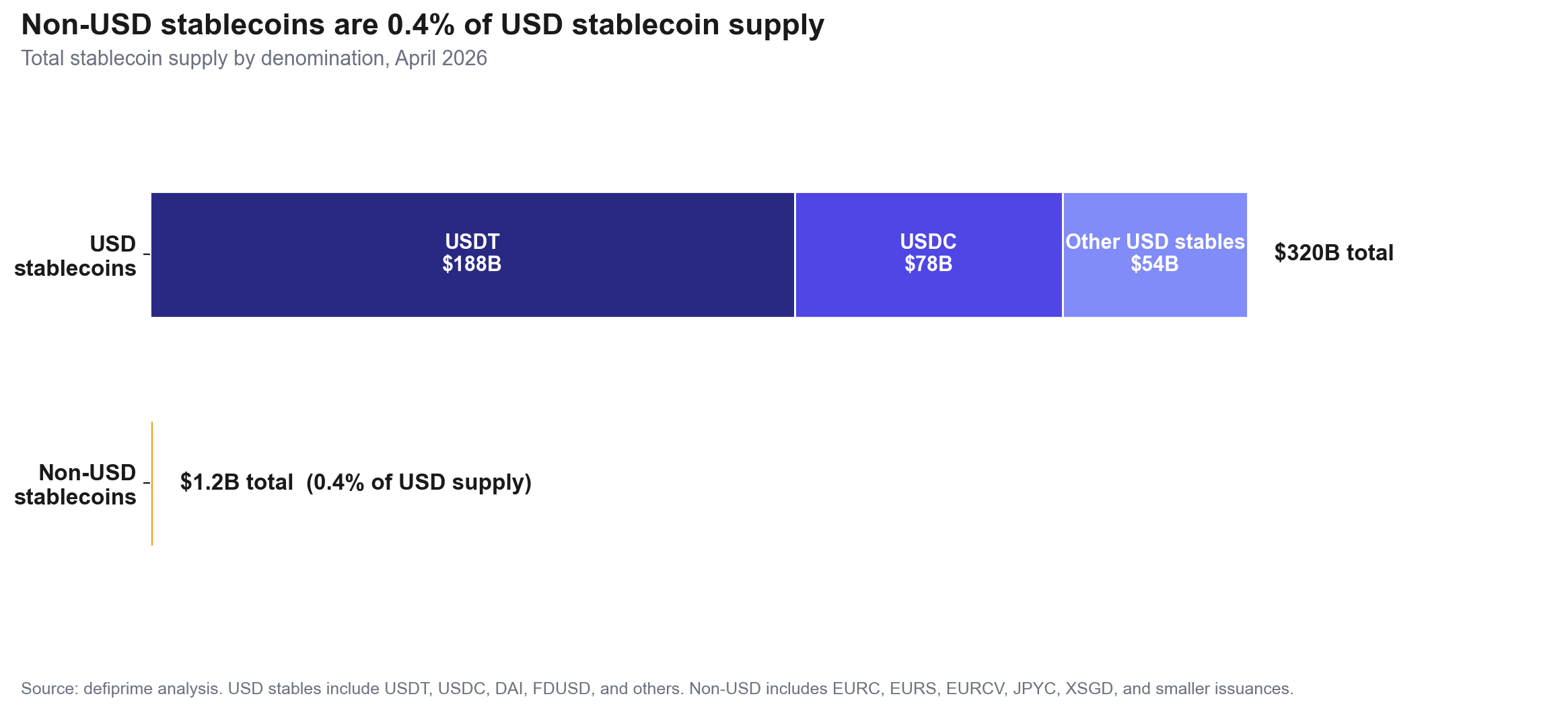

USD stablecoins clear $320B combined (USDT $188B, USDC $78B, the rest ~$54B). The entire non-USD stablecoin universe — EURC, EURS, EURCV, JPYC, XSGD, and a long tail of smaller issuances — clears $1.2B. That is a 0.4% ratio. Non-USD supply has grown roughly 2.4x over the past six months on regulatory tailwinds (EURC past $460M on MiCA, JPYC past $26M on Japanese payment-act guidance), but the gap is three orders of magnitude wide and the growth would have to compound for years just to close one of those orders.

Why this matters for forex specifically: to actually short EUR/USD as a currency position, a trader needs to borrow EUR, sell it for USD, and hold the USD. That is the synthetic equivalent of being short EUR and long USD, and it requires both legs to exist as bearer assets in deep markets. On-chain, that means a deep EUR stablecoin plus EUR lending markets or AMM pools to source the borrow. Neither exists at size. The same applies to JPY, GBP, CHF, CAD, AUD, and every other currency that has a meaningful forex pair on-chain. There is one currency on-chain at scale, and it is the dollar.

That asset-primitive gap is what forces every existing on-chain forex product into the same architecture. The venue posts a USDC margin requirement, references an external oracle for the EUR/USD rate, and settles the profit and loss in USDC. The trader never touches EUR. Neither does the protocol. The only currency that appears on the balance sheet of the venue, the trader, or the vault is the dollar, in stablecoin form. It is a clean, capital-efficient design for what it is. It is not forex.

The audience this serves is speculators betting on short-term moves in major pairs. That is a real audience and a real product. It is also a small fraction of the demand for currency exposure in the world. Corporate treasury, exporters, EM households hedging local-currency inflation, and non-USD-denominated investors all need the real currency. That is the demand volume driving the $7.5 trillion-a-day interbank market, and an oracle-settled USDC product cannot deliver any of it. No amount of HIP-3 staking, vault tuning, or oracle redesign closes that gap. The fix has to come from the stablecoin layer, and from the lending markets that would price non-USD borrow rates if they existed. Stablecoin growth alone is not enough on its own, which is the part of the standard “track non-USD supply” recommendation that needs unpacking.

Why Non-USD Stables Are Not Closing the Gap

The non-USD growth story is real and the trajectory is improving, but the structural forces working against parity with USD stables are stronger than the tailwinds working for it.

Global crypto demand is overwhelmingly demand for dollar exposure. Chainalysis’s 2025 Global Adoption work shows Brazil’s crypto flows now running 90%+ stablecoin-based, and Argentina and Colombia show stablecoins above 50% of exchange purchases. The pattern is consistent across emerging markets where local-currency inflation is doing the marketing for the dollar: users are not accumulating crypto so they can hold their local currency on a chain. They are accumulating it specifically to escape their local currency. That demand does not generate pull for an EUR or JPY or BRL stablecoin; it generates pull for USDC and USDT.

Issuer economics work in the same direction. USDC reserves earn roughly 4–5% on Treasury bills, which finances Circle’s distribution, regulatory work, and revenue share. EUR reserves earn meaningfully less than USD reserves at current rates, JPY reserves earn near zero, and most other major-currency reserves sit well below the USD yield curve. An issuer can launch a non-USD stablecoin, but the reserve yield does not pay the bills the way the USD version does. The growth in EURC and JPYC has happened on the back of regulatory tailwinds (MiCA in Europe, payment-act guidance in Japan) rather than on issuer economics, which is why the trajectory is real but slow.

Even if regulatory pressure does force non-USD supply higher, supply alone does not unlock native on-chain forex. To actually short EUR/USD as a position, somebody has to borrow EUR and sell it. That requires deep EUR lending markets at usable rates, EUR-denominated AMM pools to source the borrow, and counterparties willing to be short EUR. None of that materializes from issuer balance sheets passively holding regulatory-mandated reserves. EURC at $1B is not the same product as EURC at $1B with $300M deployed across Aave, Morpho, and Curve at competitive utilization. Today the deployed share is rounding error.

Supply is necessary but not sufficient. The binding constraint is on-chain demand for borrowing non-USD stables, and the same EM-prefers-USD pattern that suppresses demand for holding EUR or BRL on-chain also suppresses demand for borrowing them. The native on-chain FX category may simply never deepen, regardless of how much non-USD supply gets minted into existence.

Where the Off-Chain FX Audience Actually Lives

The retail forex audience that exists in size today — Pakistan, Vietnam, Brazil, Nigeria, Indonesia, the Philippines, plus offshore-US, plus the GCC — is not currently on-chain in any meaningful way. They use offshore brokers (Exness, OctaFX, FBS, Hankotrade) that already accept USDT and USDC as deposit rails at zero broker fee with sub-hour settlement. The funding-rail story is solved. Crypto is the deposit method, not the trading venue. Reaching this audience through DeFi channels is hard because crypto-Twitter and the typical DEX user demographic does not overlap heavily with EM retail forex traders, and reaching them through broker-native channels (regional affiliate marketing, Telegram, WhatsApp, local payment rails) means competing against incumbent brokers with better coverage, better deposit options, and a customer-acquisition machine that has been running for a decade.

Developed-market retail has FSCS, ICF, and equivalent broker-of-last-resort protections in place, so non-custodial is not a wedge that moves them off a regulated broker. Institutional forex is on prime brokers and ECNs (EBS, Reuters, Hotspot, FXall), where on-chain has nothing to offer at institutional scale or latency.

The audience for whom on-chain forex would be a meaningful upgrade, traders worried about counterparty risk on offshore brokers, is small, dispersed, and not currently reachable through any single distribution channel.

The Off-Chain Workaround Is the Bridge, Not the Venue

If a product wants to actually serve the audience that worries about counterparty risk at offshore brokers, the shape that works is a bridge: wallet-native UX, USDC in segregated on-chain escrow, real interbank execution at a broker-of-record on the other side. The trader gets currency exposure on real interbank quotes; the smart-contract side holds the collateral, the risk parameters, and the audit trail. The FX leg itself runs off-chain at the broker. There is no widely-known production precedent for this on the DeFi side, which is what makes it the actual greenfield.

The wedge is not “non-custodial forex.” Offshore brokers already accept stablecoin funding at zero broker fee, so the funding rail is solved. The wedge is segregation, non-seizable margin, and on-chain-provable solvency, which are balance-sheet attributes offshore brokers structurally cannot match without rebuilding their economics. SNB unpeg in 2015, FXCM’s near-collapse that same week, and a steady drip of smaller broker failures over the years since all hit the same risk: customer money on a broker’s balance sheet during a stress event. A wallet-to-broker bridge that keeps margin off the broker’s balance sheet between trades is the answer to that risk; it just is not really a DeFi product. It is a TradFi execution wrapper with a smart-contract custody surface, and a defiprime reader interested in pure on-chain primitives should treat it as adjacent rather than central.

Three Things Worth Watching in the Next Two Quarters

The category will not re-rate on stablecoin supply alone, so the supply-tracking framing that gets repeated in research memos is the wrong indicator. The signals worth watching are demand-side and pair-specific.

The first is whether a major lending market (Aave, Morpho, or Spark) opens a EURC or JPYC market with meaningful TVL ($100M+) and competitive borrow rates. Supply that sits on issuer balance sheets does not unlock anything; supply that gets borrowed at a rate close to USD borrow rates is the on-chain equivalent of the interbank EUR repo market, and that is what would actually let a venue offer a real EUR/USD position rather than an oracle bet. As of late April, EURC borrow markets exist but at TVL and rate spreads that say the demand isn’t there yet.

The second is whether any tier-one interbank market maker (XTX, Jump, a Citadel-tier shop) signs a public quoting commitment on FX pairs at an on-chain venue. Trade[XYZ]’s “institutional LP quote relaying” is a demand-side workaround, not a commitment. An MM publicly putting capital behind continuous quoting on Hyperliquid or HIP-3 is the earliest concrete signal that native FX depth is forming. None is announced.

The third is whether IBKR’s USDC funding rail through Zerohash on Ethereum, Solana, and Base scales into the SE Asia, LATAM, or MENA forex audiences currently routed through offshore brokers. If TradFi brokers normalize stablecoin deposits in EM, the deposit-rail advantage that on-chain venues currently enjoy compresses fast, and the wedge narrows to balance-sheet trust alone. The launch is US-first and the global rollout is phased.

For DeFi users, the practical takeaway is narrower than the category framing implies. Ostium and Trade[XYZ] forex pairs are real products with tight spreads on the majors, low fees, and high leverage. They work as advertised for the speculative use case. They will not turn into something larger until borrow markets for non-USD stables get deep, an interbank MM commits, or TradFi rails close the deposit-side gap. None of those is on a near-term timeline.

Treat the specific numbers above (open-interest caps, daily volumes, stablecoin supply figures) as point-in-time snapshots from late April 2026. The structural gap — one currency on-chain at scale, USD-favored issuer economics, no on-chain demand for borrowing non-USD — is the part that will not change quickly, and it is what the category is waiting on, not the venues.