In January 2026, stablecoin networks moved more than ten trillion dollars. That’s not a typo. Ten trillion in a single month.

I’ve been watching this space since 2020, and the numbers have stopped making intuitive sense. $320 billion in total market cap. Over 200 stablecoins across 37 blockchains. Monthly volumes exceeding the annual GDP of most countries. At some point you stop comparing these figures to traditional finance because the comparisons break down.

Dune Analytics released a comprehensive dataset in late February, built with Steakhouse Financial. The picture it paints is striking. Stablecoins aren’t really “crypto” anymore in the way that matters. They’re financial plumbing. The transfer volumes, the custody patterns, the velocity metrics: this is infrastructure behavior, not speculative asset behavior.

Here’s what stands out.

The History in Brief

Tether launched in 2014. For years, stablecoins were mostly a convenience for traders who didn’t want to wire money back to their banks between positions. Useful. Boring.

DeFi changed that. Between 2020 and 2021, stablecoins became the collateral layer for lending protocols, the liquidity base for automated trading, the yield-farming fuel. Circle’s USDC grew by offering more transparency than Tether, which appealed to institutions nervous about USDT’s vague reserve disclosures.

Then Terra collapsed. $60 billion gone in days. The algorithmic model failed, and the contagion pushed everyone toward fully-reserved, fiat-backed tokens. Regulators who had been moving slowly suddenly moved faster.

By late 2025, the U.S. had the GENIUS Act requiring one-to-one reserves, monthly audits, and bank charters. Europe had MiCA. The regulatory uncertainty that kept institutions away largely evaporated.

Result: $33 trillion in stablecoin transactions in 2025. $320 billion market cap in early 2026. Coinbase Institutional projects $1.2 trillion by 2028. That number seems aggressive to me, but so did current levels five years ago.

Two Issuers Control Almost Everything

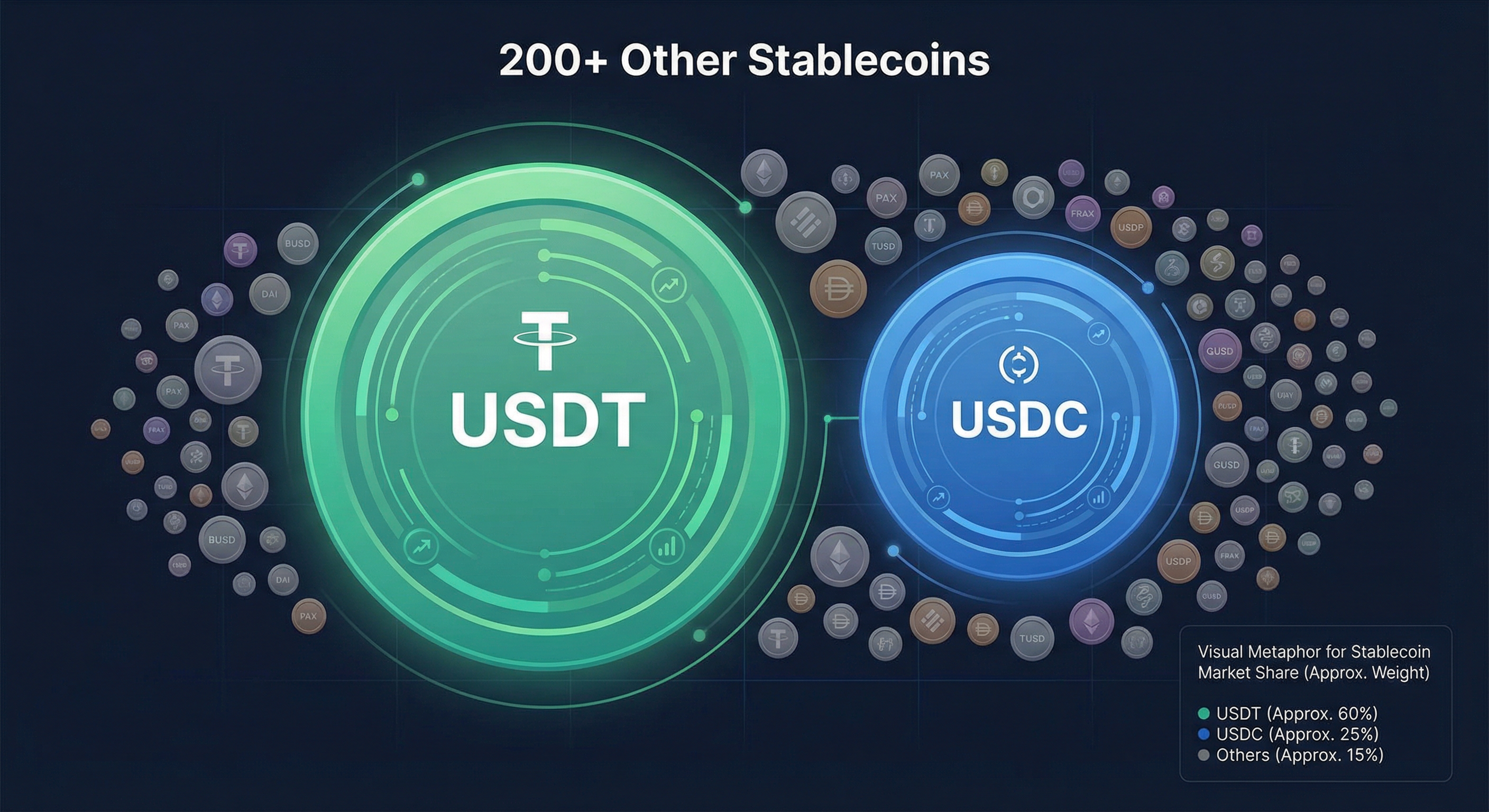

Over 200 stablecoins exist. Two matter.

Tether (USDT) has $183.7 billion in circulation, about 59% of the market. It dominates emerging markets and retail trading, especially on Tron where fees are negligible. The reserve transparency concerns haven’t gone away, but neither has the adoption.

USDC (Circle) has $75.4 billion. Smaller supply, but here’s the interesting part: USDC processed $8.3 trillion in transfers in January. USDT processed $1.7 trillion. The “regulated” stablecoin is moving five times more value despite having less than half the supply.

Together they’re 83-89% of the market depending on how you count the smaller tokens.

The rest is fragmented. Sky Dollar (USDS) at $6.9 billion. Ethena’s USDe at $6.1 billion. PayPal’s PYUSD and Ripple’s RLUSD are growing fast, but from small bases.

What does this concentration mean? Deep liquidity, stable pegs, institutional trust. Also: issuer dependency, regulatory exposure concentrated in two companies, and potential fragility if either faces a crisis. Neither collapse seems likely, but the system’s resilience depends heavily on two private companies maintaining credibility.

Holder distribution is more encouraging. Top 10 wallets hold only 23-26% of USDT, USDC, and DAI. Relatively broad. Newer tokens show 60-99% concentration, typical for early-stage products.

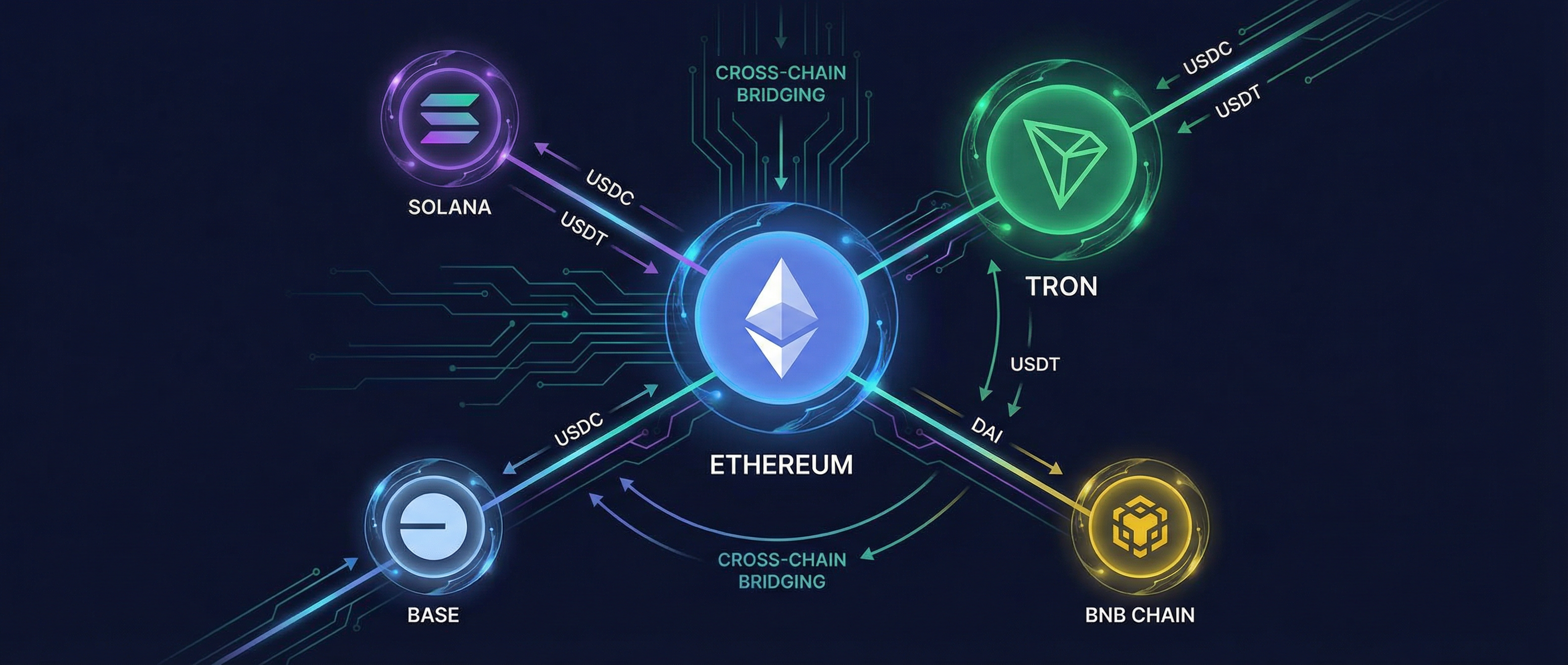

37 Chains, Uneven Distribution

Stablecoins used to mean “Ethereum.” Not anymore.

Dune tracks 35 EVM-compatible chains plus Solana and Tron.

Ethereum holds $176 billion. Still the heavyweight for institutions and established DeFi protocols.

Tron holds $84 billion. Tether’s low-fee home for retail transfers, especially in markets where cost beats decentralization philosophy.

Base, Solana, BNB Chain split the rest. Layer-2s are gaining ground as users chase lower transaction costs.

Supply and activity are different things. Base, Coinbase’s L2, led January transfer volume with $5.9 trillion despite holding only $4.4 billion in supply. USDC on Base turns over 14 times per day. On Ethereum, 0.9 times.

These differences aren’t random. High-frequency DeFi trading gravitates to cheap, fast chains. Treasury holdings and institutional custody stay on Ethereum. Yield-bearing stablecoins move slowly because holders are earning returns rather than trading.

Multi-chain expansion has clear benefits: faster transfers, lower fees, regional adoption. It also creates fragmentation and interoperability headaches addressed through bridges, wrapped tokens, and native multi-chain issuance. None of these solutions are elegant, but they work well enough.

56% of Volume Comes from Liquidity Pools

This number surprised me most.

The old story: stablecoins are for moving money between exchanges or parking capital between trades. Still true, but no longer the main event.

In January 2026, 56% of stablecoin transfer volume came from DEX liquidity pools. Roughly $5.9 trillion flowing through automated market makers, rebalancing operations, and arbitrage bots.

Stablecoins aren’t sitting idle. They’re the constant counterparty in DeFi trading. Every swap of ETH for USDC, every liquidity provision on Uniswap or Aerodrome, every flash loan (which hit $1.3 trillion in January alone): stablecoins are the stable half of the equation.

This matters because stablecoin demand is now largely internal to crypto. It’s not primarily driven by people converting fiat to buy Bitcoin. The DeFi economy generates its own stablecoin demand through trading, lending, and yield farming. More self-sustaining, less dependent on external inflows.

The center of activity has shifted from centralized order books to on-chain protocols. Centralized exchanges still matter, but marginal growth is happening in DeFi.

Centralized Exchanges Still Hold the Most

Despite DeFi’s dominance in activity, centralized exchanges hold the largest identified stablecoin reserves: about $80 billion.

Not surprising. Exchanges are the primary on-ramps from fiat. Users park stablecoins there while deciding what to buy. The $80 billion is capital ready to deploy when market conditions look right.

It also means deep order books, the ability to process large deposits and withdrawals without slippage, and significant market-making capacity.

The coexistence of $80 billion in centralized custody and $5.9 trillion in decentralized monthly transfers shows how CeFi and DeFi work together. Money enters through exchanges, moves to DeFi protocols, returns when users want fiat. Stablecoins are the common language.

172 Million Addresses

Total unique holders across the 15 major stablecoins exceed 172 million addresses. USDT leads with 136 million; USDC has 36 million.

Caveats apply. One person can have multiple wallets. Many addresses are smart contracts or exchange cold storage. But the scale indicates real network effects.

Use cases now extend well beyond trading. Gig-economy payouts in Africa and Southeast Asia. Institutional settlement of tokenized Treasuries. Corporate treasury management for global operations. Remittances that cost less and move faster than Western Union.

Dollar Dominance Gets Reinforced

Almost all major stablecoins are dollar-pegged. This extends U.S. dollar dominance into digital markets.

Stablecoin issuers are now major buyers of Treasury bills. Reserve requirements mandate holdings in cash, Fed balances, or short-term government securities. Tether reportedly holds more Treasury bills than many countries.

Large-scale stablecoin adoption creates new demand for U.S. government debt, increases dollar liquidity globally through a new channel, and extends digital dollar access to markets where physical dollars have limited reach.

The regulatory frameworks acknowledge this. The GENIUS Act bans interest-bearing “payment” stablecoins for retail users, partly to prevent deposit flight from banks. Compliant issuers can operate freely, but they can’t compete directly with bank deposits by offering interest.

The Risks Haven’t Disappeared

Reserve transparency remains an issue, especially for Tether. The company publishes attestations, but critics argue these fall short of full audits. A $180+ billion instrument without a formal lender of last resort is a systemic risk, even if failure probability seems low.

Peg stability depends on functioning markets and issuer solvency. For fully reserved stablecoins, deviations are typically temporary and correctable through redemption. But large-scale redemption events could create stress if reserves are illiquid or processing capacity can’t handle volume.

Regulatory fragmentation persists. U.S., EU, UK, Hong Kong, and Singapore frameworks differ in detail, creating compliance complexity for global issuers.

Illicit finance concerns haven’t gone away. Blockchain analytics firms estimate tens of billions in annual suspicious activity, though the vast majority of volume is legitimate. The transparent ledger actually provides better auditability than cash.

What’s Happening

Stablecoins started as a trader convenience. Now they’re a global settlement network. DeFi protocols, not exchanges, drive most activity. The use cases are financial functions that happen to run on blockchains.

This explains why stablecoin volumes have decoupled from crypto market cycles. Bear markets crush speculative tokens but barely affect stablecoin activity, because trading, liquidity provision, and payments continue regardless of Bitcoin’s price.

Banks and fintechs are entering as issuers. Multi-currency stablecoins will eventually grow beyond USD dominance. Tokenized real-world assets are creating new yield opportunities. Programmable payments, still nascent, are becoming possible.

USDT and USDC combined market share is beginning to slip as new entrants gain traction. PayPal’s PYUSD, Ripple’s RLUSD, and yield-bearing options are carving niches. Network effects favor concentration, so the duopoly probably persists, but competition is increasing.

If projections hold, stablecoins could hit $1 trillion within a few years. At that scale, they become a systemically important part of global finance, with all the regulatory attention that implies.

What the Data Shows

The Dune dataset confirms what anyone watching closely suspected: stablecoins have reached a scale where they’re no longer experimental.

$320 billion in market cap. $10 trillion in monthly transfers. 56% of volume through DeFi. 172 million holder addresses. Two issuers controlling 85% of supply while over 200 alternatives compete for the rest.

The infrastructure exists. The regulatory frameworks are in place. Institutional adoption is happening. Whether this is the “future of money” or just a new layer in the existing financial system is mostly semantic. The practical reality: stablecoins move significant value, and volumes keep growing.

The January 2026 data doesn’t suggest a sector about to stall.

Data: Dune Analytics Stablecoins Overview (February 2026), DefiLlama, Steakhouse Financial on-chain analysis.