Disclosure: This article was sponsored by FinNexus

Hello! What’s your background, and what are you working on?

Hi there, this is Ryan Tian. Along with Boris Yang, our CEO, I am the co-founder of FinNexus, as well as our in-house financial expert. I’ve been working in traditional finance for a decade before moving into crypto, and it’s been quite a ride!

Creating a platform from scratch is no joke, even when you have a committed team behind you as we do. With FinNexus, you have to add the challenge of dealing with what is essentially unexplored territory - we are one of a handful of platforms offering options trading in Decentralized Finance.

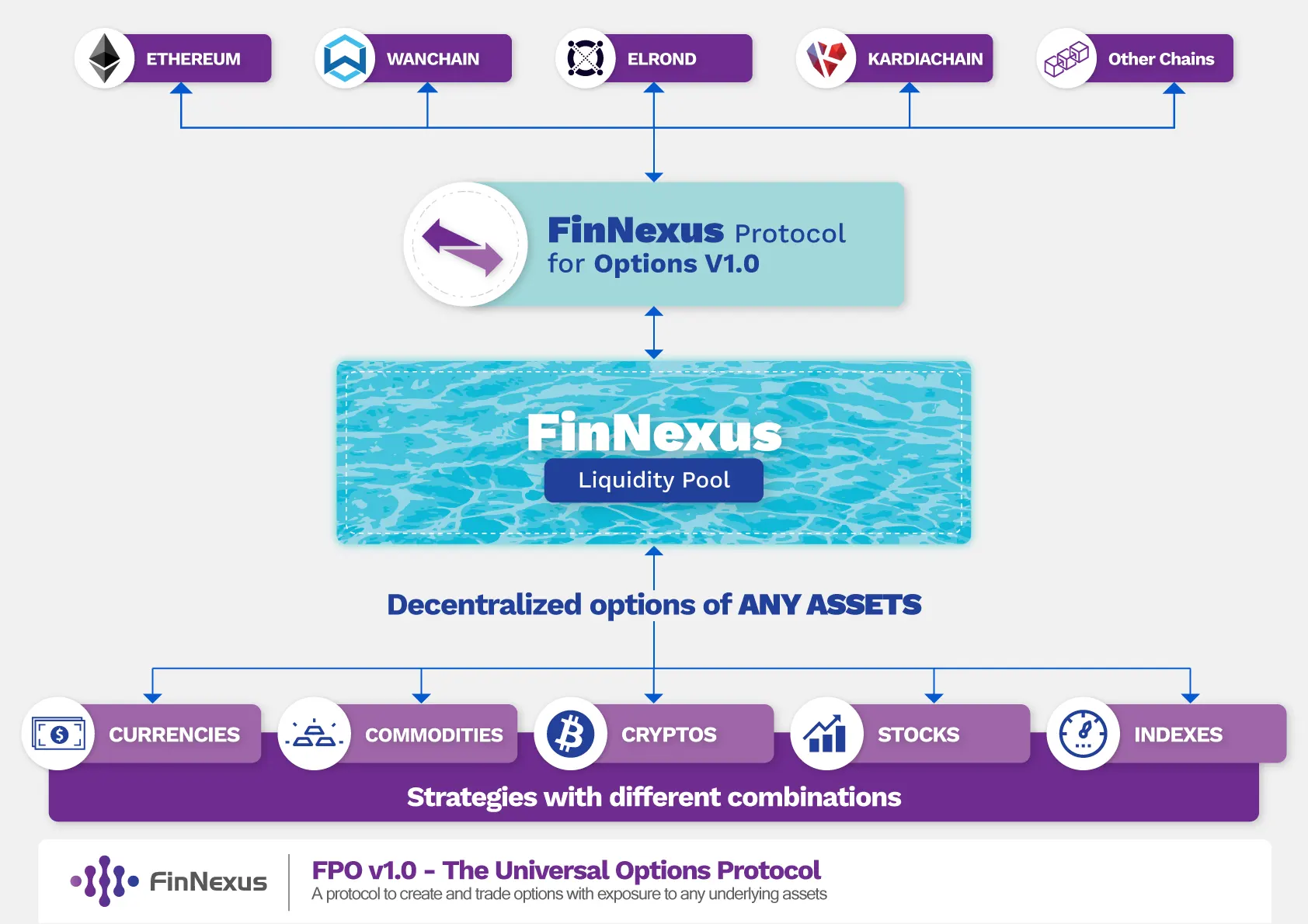

At the moment, FinNexus has two key products - the FinNexus Protocol for Options (FPO) and our mining and staking service. The FPO allows users to write, buy and settle options using a pooled liquidity system, which spreads out risks and allows participants to share premiums. This makes trading both more intuitive than on traditional options platforms and partially solves the issues of liquidity - or rather the lack of it.

Mining and staking are also core elements of our offer. We have two pools - plus one for algorithmic stablecoin FRAX, more on it later - and we have recently overhauled our system, launching a dual mechanism that rewards users for mining USDC/USDT and FNX in pairs. By choosing the right token combination and staking their funds for long enough, users can reap up to 320x multiplier. The mechanism was created to avoid situations where miners would simply farm and dump FNX, something we obviously think would not be healthy in the long run.

What’s FinNexus backstory?

FinNexus has been built for DeFi since its birth. When I was an investment banker, I was involved in dealing with all kinds of financial derivatives - and yet to this day, the power of derivatives never ceases to amaze me. At the time, I thought: “What if we can bring derivatives to DeFi?”

Options are perhaps the most important derivatives in traditional finance and attract great volume. After multiple brainstorming sessions and discussions, we decided to start with decentralized options.

The idea was powered by the FinNexus team - a group with different expertise, financially supported by early believers. Boris, the CEO and a blockchain veteran, and I mainly designed the platform’s structure, while Crane and Jia, with over 15 years of coding experience in tech, lead the developers’ team in programming.

Recently, apart from options, the team has started to build another derivative product – decentralized leveraged tokens, which is expected to come to fruition in the second quarter of 2021.

FinNexus’ goal is to introduce traditional financial derivatives into the DeFi market while innovating with brand new models that have never been seen in traditional finance before.

What went into building the FinNexus?

We started working on FinNexus in 2019 but really got up to speed the following year, when the platform went live and we launched our social media channels. Since then, we kept on adding products and tweaking existing ones, but our key product has remained the FinNexus Protocol for Options (FPO), a decentralized, non-custodial system for writing, trading, and exercising options currently on Ethereum and Wanchain. (We are planning to deploy it on other chains, too.)

The protocol serves both options buyers and sellers. Buyers can buy contracts without hassle, setting their desired options terms without worrying about liquidity depth or slippage. As we deal in American options, holders can exercise anytime before the expiry.

Meanwhile, sellers have access to safe and stable rewards, without having to hedge against the risks of the specific option - which could require significant expertise - as the protocol itself automatically diversifies risks. The entire system has been checked not just by our team of engineers, but also audited by Peckshield.

The system is powered by the FNX, our own token - which, even though it has recently touched its all-time high, is considered undervalued by many in the community. FNX is a payment medium, settlement medium, and collateral. It is also instrumental in liquidity mining, governance, and more. In mid-February, we had a huge burn of 290,000,000 FNX. Roughly 60 percent of our total supply was eliminated. This was done to reassure investors that tokens from our non-circulating supply would not be dumped on the market in the future.

What’s your business model?

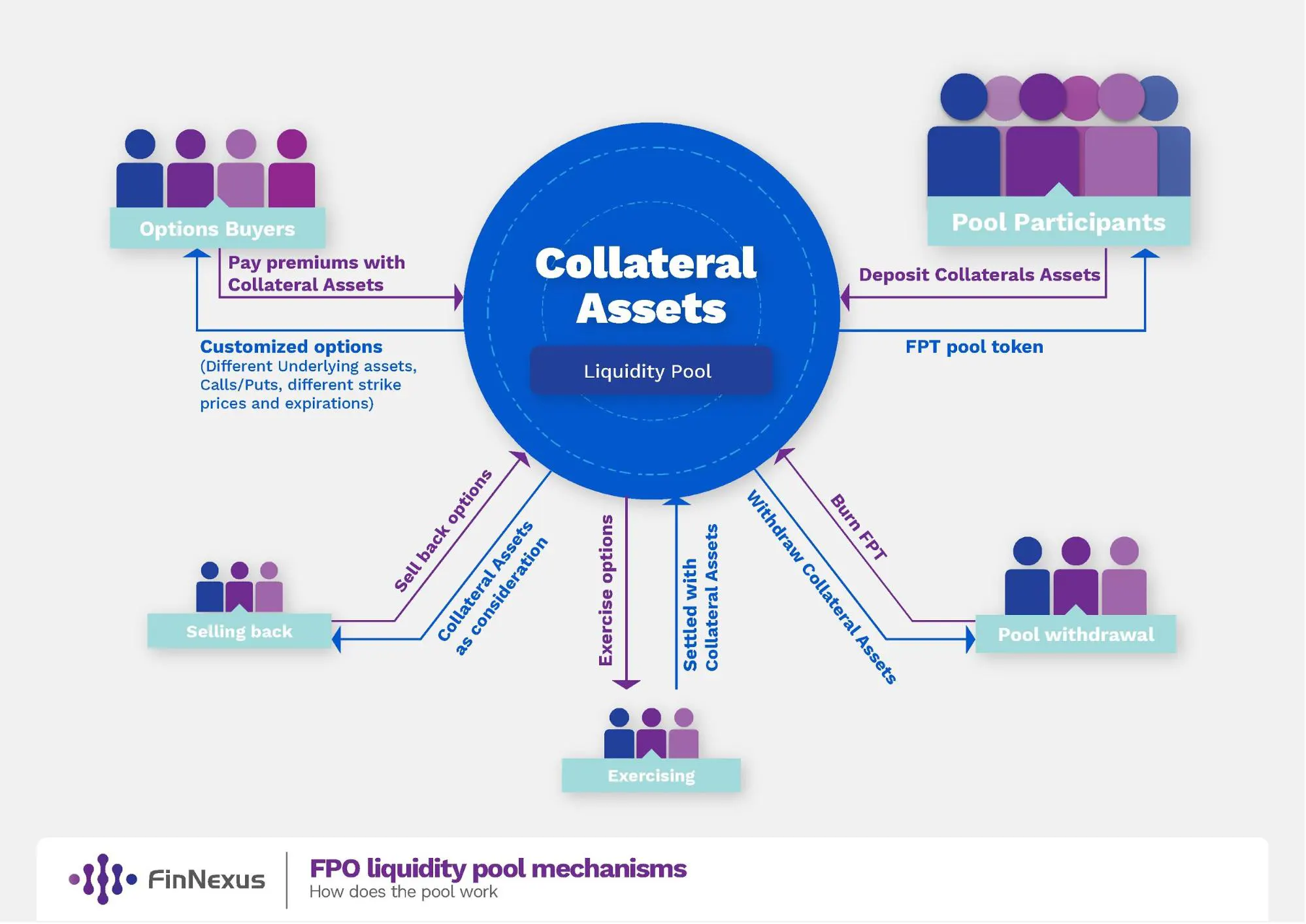

Liquidity pools are the heart of the FPO model.

- Liquidity pools are also collateral pools, working as the counterparty to all the options, with any variety of terms, written from that pool.

- One pool can power different options with various terms simultaneously. Risks are diversified and premiums are shared automatically.

- Liquidity is collectively shared with all the buyers, and options are traded with little price slippage.

- The pools provide constant liquidity for options transactions. The market for a specific option does not need to be terminated or rebuilt when the contract expires. Liquidity providers do not need to worry about rolling their liquidity to another pool at expiration.

- This model provides flexibility for option buyers, who can literally tailor their options terms according to the needs.

- Interfaces can be designed to be simple and easy to operate for new users.

- Pool participants are collected together in the pool as options writers. Due to this, there may be risks if the market makes dramatic movements that are unfavorable to the options sellers. You can have a look at our simulation for the financial behavior of the collateral pools.

I wouldn’t say that there is any competition now in the DeFi derivative market, as it is just getting started and the potential is huge. I have the major participants covered in 3 of my previous articles (1 2 3).

Many tend to compare us with Hegic as we somehow share a similar logic in terms of pooled liquidity model. Still, there are some significant differences.

Pool compositions

- Hegic has two pools with WBTC and ETH as collaterals. Each pool powers contracts with corresponding underlying assets. Options are purchased and settled in WBTC and ETH.

- FinNexus has two pools on Ethereum, with USDC/USDT and FNX as collaterals. Options are purchased and settled in the related collateral asset. FinNexus’s pool deploys a MASP (Multi-Asset Single-Pool) mechanism, which allows hybrid assets as collaterals, like in the USDC/USDT stable coin pool. The choice for payments is more flexible. The FinNexus team is planning to add more types of assets as collateral in the future.

Underlying Assets for Options

- Hegic options’ underlying assets are currently WBTC and ETH. Both WBTC and ETH calls and puts have deep liquidity.

- At present, FinNexus supports five crypto assets as underliers, although the MASP mechanism allows for potentially unlimited types of assets to be added, including commodities, stocks, fiats, indexes, etc. Settlement takes place in stablecoins and in this regard, the system is more in line with trading conventions.

Pool Risks

- With Hegic, because WBTC and ETH pools are separated to power the corresponding options, risks are somehow more concentrated and more likely to be hedged for liquidity providers. An auto hedging mechanism is under construction.

- On FinNexus, with more diversified underlying assets, together with a risk adjustment parameter for options pricing, liquidity providers’ risks are more diversified. The platform is designed to automatically dilute risks with its universal pooled-liquidity mechanism. Moreover, FinNexus introduced a risk-adjustment parameter, to act as an AMM mechanism and better balance the distribution of puts and calls in the pool.

Options Pricing

- FinNexus applies Black-Scholes Model in pricing options and programs it in smart contracts. IV, as the most important parameter in pricing, is fed into the protocol. Volatility surface is also derived for different strikes and expirations.

- Hegic applies a simplified options pricing model, and the pricing parameters are manually adjusted according to the average IV from Skew.

What’s your position on the regulatory landscape today?

The regulatory landscape is obviously pretty slim in DeFi. Part of it comes down to just how new everything is in this field, so it is normal that the authorities take time to catch up. I also think that this lack of supervision is part of what makes DeFi and crypto more generally attractive to many users.

But for healthy growth, some control will be necessary - and is probably going to come in the future. At FinNexus we would not mind it. If you are a legit project and provide real value to users, why being afraid?.

What are your goals for the future?

FinNexus aims to become the one place where options traders interested in DeFi will go by default. Our recent performance has been very encouraging, with the Total Value Locked skyrocketing by more than 12 folds between late January and mid-February, while FNX set successive new all-time highs. Yet, we are still seen by many as an undervalued project - this is both flattening, encouraging, and challenging because we need to keep on delivering results.

In the immediate term, what we are really focusing on are two things. First, we need to increase liquidity. This is an issue that many new projects have in common - you need liquidity to power up the platform and oil cogs of your trading mechanism so to speak. We are quite satisfied with the increase in TVL so far, though we believe much more can be done. The second goal is to create an array of products to complement our basic trading offering. We are working on an insurance system for our USDC/USDT pools and have been in talks with Frax Finance to create an algorithmic stablecoin pool - this would bring further innovation to FinNexus and would allow us to tap into that growing market.

If you look at the challenges, there are plenty, from getting our platform mainstream to keeping up with new developments. But that’s what you would expect from being in a completely new space, isn’t it?

What are your future thoughts for the DeFi market?

We obviously are very optimistic, otherwise, we would not be here in the first place! I think what we are seeing in the DeFi market these days is very encouraging. There is talent, there is a willingness to find out new solutions to old problems and, increasingly, there is money to do so. As Bitcoin becomes popular, yield-hunters and innovators are likely to move to Decentralized Finance. Then, of course, there are risks and no doubt many of the projects you see today may not be there a few years from now, that is part of working on a new frontier.

Looking at options specifically, the potential is massive. It is no mystery that derivatives are increasingly popular with retailers in legacy finance, where several platforms work with options. A recent piece by the Economist reported that last year almost 30 million equity options were traded each day on American exchanges. That’s 50 percent more than in 2019. If you look at the current volumes, it would only take a fraction of those funds to move to DeFi for it to really boom.

Where can we go to learn more?

Please feel free to check:

- Our blog: https://finnexus.io/blog

- Our medium Channel: https://medium.com/finnexus

- Twitter: https://twitter.com/fin_nexus

- Telegram: https://t.me/FinNexusOfficial

- Our docs repository: https://www.docs.finnexus.io/