Decentralized finance (DeFi) is quickly gaining momentum as an area of application for distributed ledger technologies.

DeFi refers to a movement started by a group of projects building financial products and services on the Ethereum blockchain to promote their work and encourage the development of an open financial system. Although DeFi is inherently platform-agnostic, it has grown to become the most popular use case for Ethereum.

Returns on DeFi lending products have been impressive relative to the benchmark for returns on other asset classes. This has led many to wonder how those in traditional finance will view DeFi, but before we compare the two, let’s start with a look at how DeFi came to be.

The origin of DeFi

Although projects like Bitcoin could be considered DeFi products, the birth of DeFi as a movement can be attributed to the launch of the Dai stablecoin by MakerDAO. Dai and other stablecoins like USD-Circle (USDC) are cryptocurrencies (like Bitcoin) whose value is pegged to something for stability; in this case, the U.S. dollar. Some stablecoin systems simply accept deposits of currency and issue tokens in exchange, but what makes Dai interesting is the fact that it’s minted using collateralized debt positions (CDPs) created on the MakerDAO platform.

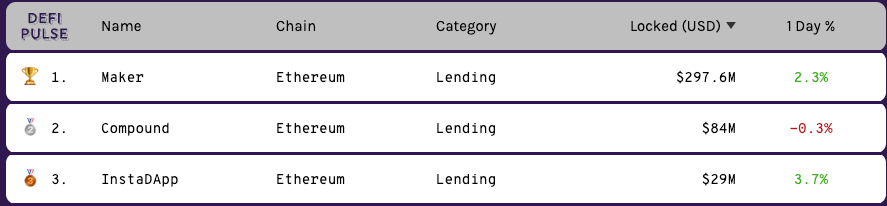

MakerDAO allows users to deposit Ether, the cryptocurrency associated with the Ethereum smart contract platform, and mint up to 66% of the value of Ether in Dai. Why would anyone put down $100 to get $66 back? Because they don’t lose the $100 worth of Ether (unless the value drops enough to cause a margin call) and that extra $66 can be used on other financial opportunities. It can be used to buy Ether and create another CDP, trade other assets, or be lent to other speculators for interest using platforms like [Compound}(https://compound.finance/).

At the time of writing, 1.29% of the supply of Ether has been locked in MakerDAO CDPs at an overall collateralization ratio of 378%. Having a platform that offers an over-collateralized, dollar-pegged stablecoin that anyone can use without having to trade actual dollars using cash or bank accounts provides a decentralized way to create and use dollars. This is the reason Dai has become the backbone of many of the applications currently being developed in DeFi.

To better understand how lending products in DeFi compare with investment opportunities in traditional finance, this article provides an overview of existing asset classes and their expected returns along with a summary of the products being developed in DeFi and their performance so far.

Traditional asset classes and returns

When reviewing returns on different asset classes, it’s important to keep in mind that fiat currencies grow at different inflation rates. Subtract the annual inflation from the returns offered by different investment products to get a better picture of how annual returns compare with the annual loss in purchasing power that comes with inflation. For example, inflation in the U.S. averages around 2%, so any investment offering less than a 2% annual return actually leads to an overall loss in the value of the portfolio.

Cash - 0.01% to 2.50%

Cash refers to both physical currency and electronic liabilities that can be easily accessed (savings, checking, and money market accounts). Holding cash generally means losing purchasing power to inflation but keeping it in certain types of accounts will allow the depositor to collect interest.

Regular checking and savings accounts rarely offer interest approaching anything substantial, but high-yield savings money market accounts will typically allow the depositor to at least keep up with inflation. A regular savings account right now stands at 0.01% annual interest. High-interest savings and money market accounts that may require a higher minimum deposit average between 2.00% and 2.50% annual returns, roughly on par with the inflation of the U.S. dollar.

Commodities - from negative yields to 18%

As an asset class, commodities refers to the trade of goods, including livestock, agricultural products like corn and soybeans, energy, and precious metals. Trading commodities predates the trade of stocks and bonds and provides a helpful way to diversify portfolios beyond stocks and bonds. There are a number of different ways to trade commodities, from day trading or investing in specific markets to trading options or futures and investing in ETFs.

Commodities yield different rates of return based on the class of good being traded and the type of investment product used to gain exposure to the good. For example, gold has traditionally provided a “safe haven” during economic downturns, but with the emergence of cryptocurrency as an asset class, many have started to wonder whether or not the fact that gold costs money to store and doesn’t yield dividends may change that perception.

Bonds / Fixed Income - 0.25% to 2.70%

Bonds provide investors with a set interest rate on their investment. The investment rates offered fluctuate based on the federal funds rate that determines the interest rate at which banks and credit unions lend each other excess reserves and the current rate of inflation in the money supply. Because they provide a fixed return, rates tend to provide less upside than riskier investments like stocks and foreign currencies.

Most government bonds offer between 0.25% and 2.5%. Bonds can also be traded and packaged into derivatives like index funds for more speculative opportunities and greater potential upside. Indicies tend to provide returns ranging from 2.5% to 13%, but this article cites the average return on bonds themselves to distinguish between speculative and fixed investments.

Foreign Currency - returns varies

Foreign currency, more commonly referred to as foreign exchange (FX), includes roughly 95% of speculative investment. In the strict sense of the word, cryptocurrency can be considered an emerging asset class within FX. FX can be traded at any time and requires less capital up-front than many other assets. Trading FX is similar to day trading stocks in that it’s typically done over short periods of time (minutes, hours, or days) and most traders only disclose their earnings to tax collectors, so it’s impossible to provide an average return.

As is the case when day trading stocks, the amount of experience and capital a person or organization has when trading FX can lead to very different returns. For example, someone with a lot of capital but not much experience might get lucky with a decent strategy and make more money than someone with more experience and less capital who has a great strategy.

Real Estate - 9.50% to 11.80%

Real estate investments come in a wide variety, from “house-flipping” trailers, suburban homes, and mansions to developing rental or commercial properties. Investing in real estate generally requires more capital and know-how to get started. According to Investopedia, the average 20-year return on commercial real estate is around 9.5%, with residential and diversified investments averaging 10.6% and real estate investment trusts (REITs) at 11.6%.

These numbers provide a helpful reference, but different approaches to investing can yield very different results. Someone might luck into a great deal on a tax foreclosure and purchase a property for $3000 they can then turn around and sell at market rates of $50,000 or more. Such opportunities may be rare, but they do exist and contribute to FOMO around highly speculative investments like real estate.

Stocks - 8% to 10%

Stocks also called “equities,” represent shares of ownership in publicly-traded companies. Different people invest in stocks with the expectation of making money in different time frames. Investing in equities provides short-term volatility for day traders and has historically outperformed other asset classes from the perspective of long-term investment. These approaches require different strategies, so the return on investment for day traders will be very different than the returns seen by those making long-term investments.

The S&P 500, comprised of the 500 largest publicly-traded companies in America, averages about a 10% return per year. Passive investors who hold stocks for retirement and favor basic products like index funds hope to see an average of 10% per year.

Returns for traders, on the other hand, can fluctuate wildly. Research shows that active traders who don’t maintain diversified portfolios tend to lose money. A disciplined trader who’s found an effective trading strategy may see 5% to 10% returns per month, but the strategy could also stop working at any time. Those who start with more capital can employ different trading strategies than someone starting out with $100,000 or less and experience weighs in as well so it’s difficult to predict the returns an average person could make from day trading.

Infrastructure - 5% to 10%

Infrastructure is an often-overlooked asset class that combines many of the elements involved in investing in other asset classes. Infrastructure includes large-scale projects led by governments or government-regulated monopolies or smaller projects that tend to be created by private firms or grassroots organizations. Projects may be funded publicly, privately, or through public-private partnerships.

Investing in infrastructure typically means buying stock in companies that own and operate infrastructure for transportation, commodities, or data. Like commodities, investments in infrastructure tend to be made to diversify and preserve the value of portfolios rather than being expected to provide generous returns. Investing in infrastructure tends to yield slightly better returns than stocks and provides less volatility as well. While it isn’t unheard-of for infrastructure projects to fail, the fact that they’re usually overseen by the public sector helps mitigate the risk involved with investing.

DeFi Asset Classes and Returns

Anthony Sassano, Product Marketing Manager at Set Protocol and Co-Host of the Into the Ether podcast, explains that

“…the returns in DeFi have so far been much better than traditional finance (especially in lending markets). The rates for lending stablecoins on Compound/Dharma or dYdX are consistently between 10% and 20% APR. This is what you get when you remove a middleman.”

DeFi products currently provide opportunities for loans, margin trading, and algorithmic trading.

Loans - 10% to 20%

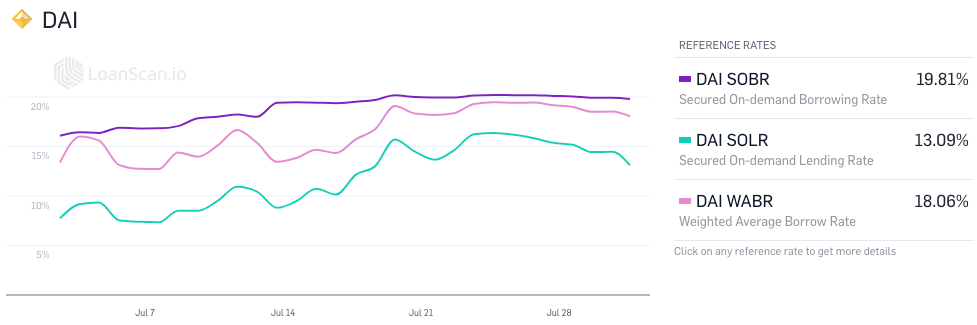

Cryptocurrencies can be borrowed and lent using platforms like Compound and Dharma, and stablecoins like Dai and USDC provide the highest returns by far. DeFi analytics platform LoanScan currently (July 31, 2019) displays a reference rate of 13.56% interest on Dai and 9.21% on USDC. Part of the reason that lending products in DeFi have been able to offer such impressive returns on stablecoins is because it provides liquidity for traders capable of making higher returns on cryptocurrency than traders in traditional markets. For a great report on the landscape of digital asset lending, check out the DeFi Series by Binance Research.

Algo and Margin Trading - returns varies

As is the case with day trading in traditional markets, most traders only report their earnings for tax purposes and many DeFi products for algorithmic and margin trading haven’t been around that long, so it’s difficult to get a sense of the possible returns. Products are only starting to be developed in this category, but dYdX is a popular example that provides a decentralized exchange with up to 4x margin trading.

Another is Set Protocol, who recently launched their first tokenized trend-trading product. Tokenized trend-trading allows investors to purchase a token that algorithmically executes a trend-trading product. In certain jurisdictions, this enables traders to gain exposure to the execution of trading strategies without accruing the taxes that would come with capital gains and loss if they actually executed those trades manually.

Conclusion

DeFi began with the development of protocols for decentralized exchange, stablecoins, and basic applications for loaning and gaining interest on stablecoin deposits and is growing to encompass a variety of applications. Whether or not DeFi products will continue to offer superior returns on lending and how the world of traditional finance will adopt and react to DeFi remains a mystery, but the dream of creating an open financial network will continue to drive the development of infrastructure for decentralized technologies.