If you follow DeFi at all, you’ve noticed it’s gotten more complicated. Not in a bad way, necessarily, but the space is importing structures from traditional finance that would have seemed absurd two years ago. One of the more interesting imports is tranched credit markets, which split lending pool risk into layers so different investors can take on different levels of exposure. As of March 2026, these aren’t experimental anymore. They’re becoming core infrastructure on EVM chains and Solana.

How tranching works

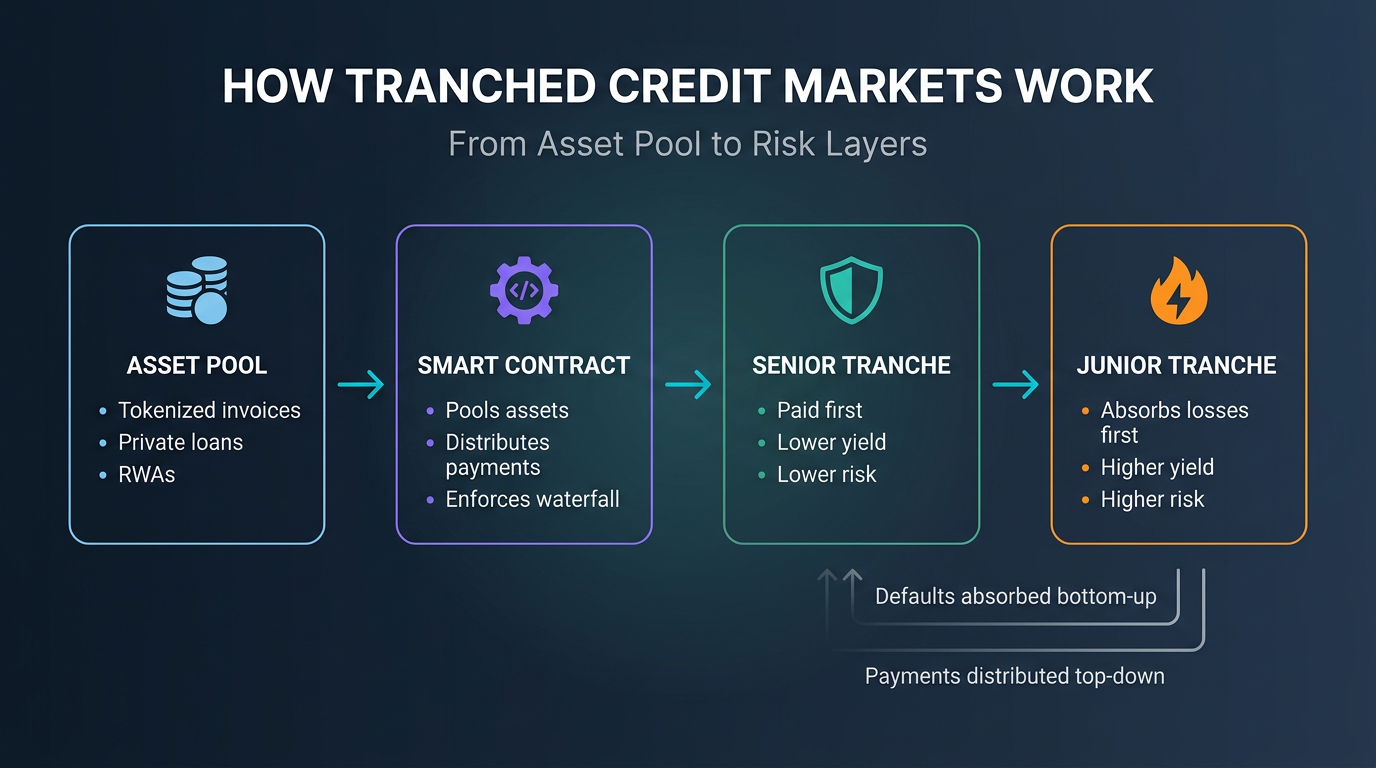

Think of a lending pool split into layers. The senior tranche gets paid first and offers lower, steadier yields, while the junior tranche absorbs losses first but earns more when things go well. This is borrowed directly from TradFi securitization, the same basic idea behind mortgage-backed securities from the 1980s. The difference is that smart contracts handle the mechanics here, pooling assets like tokenized invoices or private loans, distributing payments top-down, and absorbing defaults bottom-up. What makes this interesting in a DeFi context is the composability angle: tranche tokens can be traded or used as collateral in other protocols, so a static loan becomes something you can actually do things with.

DeFi outstanding loans grew 37% in 2025, mostly driven by RWA tokenization and institutional demand for yield, and in 2026 the conversation has shifted toward scalable models incorporating AI-driven credit scoring, cross-chain interoperability, and programmable collateral.

Who’s building on EVM chains

EVM chains, meaning Ethereum and L2s like Arbitrum, Optimism, and Polygon, are where most of this work lives. The composability helps, and institutions are more comfortable here. Here’s a quick-reference breakdown of the protocols worth knowing, followed by some context on how they cluster together.

| Project | Chain(s) | Core focus | Latest (March 2026) |

|---|---|---|---|

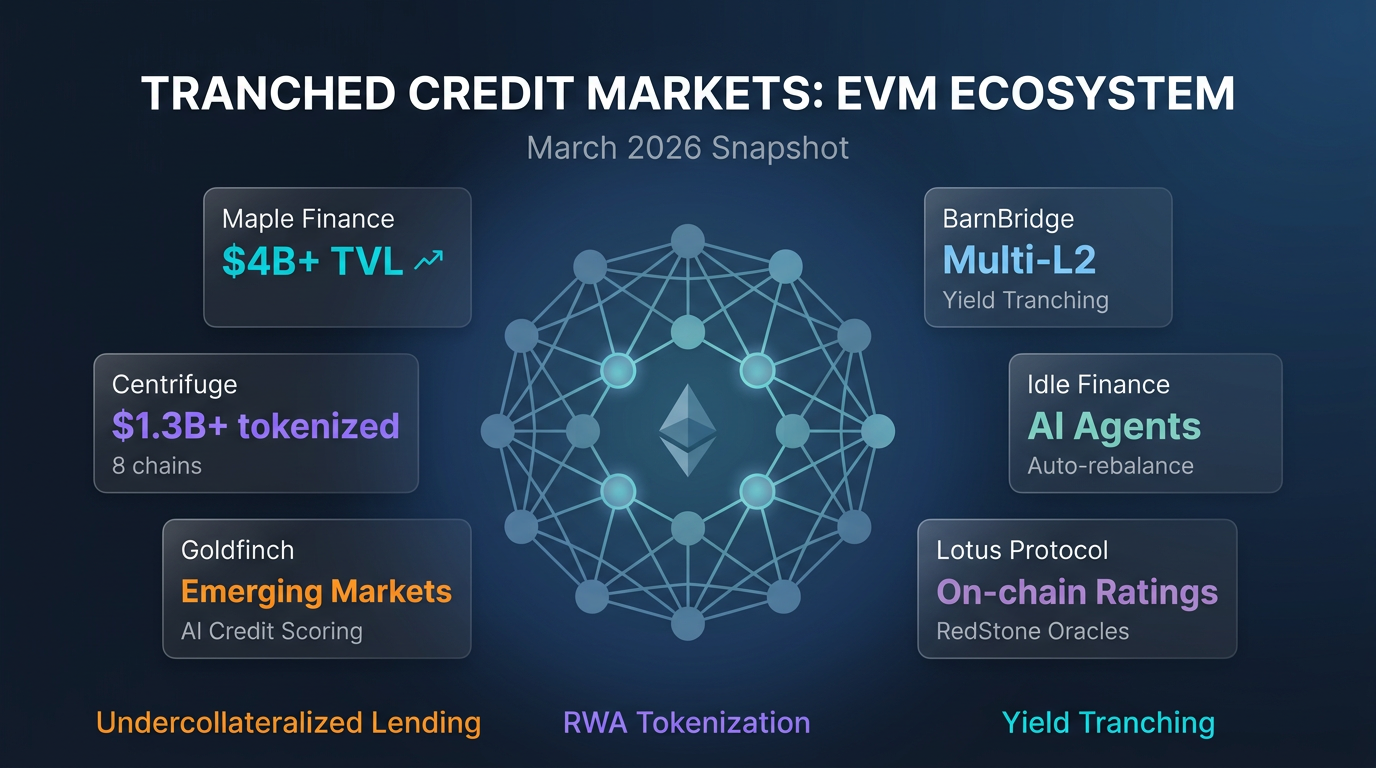

| Goldfinch | Ethereum | Undercollateralized loans to emerging markets via tranched pools | TVL holding steady amid RWA boom, integrated AI-driven credit scoring for junior tranche protection |

| Centrifuge | Ethereum (EVM-native since V3) | Tokenizing RWAs into tranched liquidity pools | Expanded to 8 chains via V3/Wormhole, over $1.3B in tokenized assets distributed per RWA.xyz |

| Maple Finance | Ethereum, Solana, Arbitrum | Institutional overcollateralized loans with senior/junior tranches | Outstanding loans grew eightfold to ~$1.5B in 2025, TVL surpassed $4B, syrupUSDC integrated across major DeFi protocols |

| BarnBridge | Ethereum, Arbitrum, Optimism, Polygon | Yield tranching for DeFi pools | Focusing on stablecoin-backed credit, aligned with programmatic payment trends |

| Idle Finance | Ethereum, Polygon | Perpetual yield tranches with auto-rebalancing | Yield optimization with AI agents for tranche management |

| Strata Protocol | Ethereum (expanding) | Risk-tranching for yields and RWAs | Dynamic splits integrated with Pendle, srUSDe in high demand for reserves |

| TrueFi | Ethereum | Uncollateralized lending with tranched pools | Flat growth, exploring AI for default prediction |

| Pareto Credit | Ethereum (Morpho-integrated) | Structured vaults for institutions | KYC-gated composability, partnering for cross-chain credit markets |

| Lotus Protocol | EVM (various) | Tranched credit with on-chain ratings | Integrating RedStone oracles for dynamic vaults, generating buzz in crypto circles |

These protocols fall into a few clusters. On the undercollateralized lending side, Goldfinch has been at it the longest, making loans to emerging markets. TrueFi takes a similar approach, though growth has stalled. Maple Finance pivoted to overcollateralized lending after its 2022 difficulties and is probably getting the most institutional attention of the group right now, with outstanding loans growing eightfold in 2025 and TVL passing $4B by year-end. Separately, Apollo Global Management signed a deal in February 2026 to acquire up to 90M MORPHO governance tokens over 48 months, a sign that major asset managers are building direct stakes in DeFi lending infrastructure.

The RWA tokenization cluster is led by Centrifuge, which migrated to an EVM-native architecture in 2025 and now operates across 8 chains including Ethereum, Base, Arbitrum, and Solana. They’ve distributed over $1.3B in tokenized assets according to RWA.xyz. Pareto Credit is working a similar angle through structured vaults on top of Morpho. Then there are the yield-tranching protocols: BarnBridge across multiple L2s, Idle Finance experimenting with AI agents, and Strata Protocol doing dynamic splits with Pendle. Lotus Protocol is newer but worth watching for its on-chain ratings approach and RedStone oracle integration.

The RWA wave underneath all of this is real. BlackRock and Apollo are participating, and some estimates put the DeFi market at $100B valuation by year-end, roughly double 2025.

Solana’s side of the story

Solana’s speed and low fees make it appealing for DeFi broadly, but tranched markets are less mature here. DeFi TVL is approaching $10B (down from a September 2025 all-time high above $12B), with RWAs and private credit among the growing segments.

| Project | Chain | Core focus | Latest (March 2026) |

|---|---|---|---|

| Credix Finance | Solana | Tokenizing private credit into tranches | $26M outstanding, focused on USD-denominated emerging market debt including Latin America and Asia |

| Tranched.fi | Solana | On-chain securitization with auto-tranches | a16z-backed, institutional-grade RWAs, real-time tranching for fintech lenders |

The two main players tell different stories. Credix has been around longer and focuses on emerging market debt in Latin America and Asia, while Tranched.fi is newer, better funded, and building for fintech lenders specifically.

Solana’s 2026 roadmap matters for this space because Alpenglow (faster consensus) and Firedancer (execution integrity) should help tranched markets handle stress better. Kamino and Marginfi already offer modular lending, but explicit tranching is still ramping up. J.P. Morgan issuing commercial paper on Solana is a signal worth noting. That said, the ecosystem is still absorbing lessons from security incidents, most notably Step Finance’s ~$29-40M breach (estimates vary) in January 2026 that led to their permanent shutdown, a reminder that newer ecosystems carry real risk.

What tranching actually solves

The core value is letting different investors choose their risk exposure, so a pension fund can take the senior tranche while a higher-risk investor takes the junior. This widens who can participate in DeFi lending considerably. It also addresses the overcollateralization problem that has plagued the space, where traditional DeFi lending requires 150%+ collateral and locks up capital that could be doing something productive. Tranching gets around that by layering risk instead of brute-forcing safety through excess collateral.

On a practical level, tranche tokens being tradable and composable helps with liquidity, and regulatory clarity in 2026 is making banks more comfortable participating, especially around programmable stablecoins and cross-border flows. Because everything runs on-chain, the payment waterfalls and default mechanics are visible to anyone who cares to look. Some protocols are already running AI agents that approve loans in under 200ms, which would have been science fiction in DeFi even a year ago.

What could go wrong

I’d be dishonest if I didn’t flag that tranching has a mixed history. The 2008 financial crisis was, in large part, a story about tranched products where complexity obscured real risk, and some of those lessons apply directly here. Correlated defaults are the big concern: if enough borrowers default at once, even senior tranches take losses, because the junior tranche that’s supposed to absorb hits has limits. Oracle quality matters too, since bad price feeds or inaccurate credit data can throw off valuations system-wide.

Smart contract exploits remain a real threat, as Solana’s recent history shows. The regulatory picture is murky in places, since mixing pseudonymous DeFi participants with KYC-compliant RWA issuers creates tension that regulators are watching closely. And junior tranches can become illiquid fast during market stress, exactly when you’d most want to exit. Better oracles, more audits, and reinsurance mechanisms for junior tranches would help, but these risks aren’t theoretical.

Where this is heading

The crypto-collateralized lending market reached $53B by mid-2025 according to Galaxy Research, with DeFi protocols capturing roughly two-thirds of that volume, and RWAs are going mainstream through tokenized funds, private credit markets, and consumer-facing apps. Lotus Protocol’s tranched vaults with full oracle stacks are worth tracking, and as traditional banks lose ground to private credit, on-chain tranching is picking up slack.

Whether tranching delivers on the promise of scalable undercollateralized DeFi lending is still an open question. The infrastructure is better than a year ago, and the institutional interest is real, but so are the risks. I keep coming back to the fact that the 2008 analogy isn’t just rhetorical, it’s structural, and the space will need to prove it’s learned from that history rather than just repeating it on faster rails.