Crypto launchpads have a trust problem. The basic pitch, “give us money and we’ll build something,” has been repeated so many times, with such consistently disappointing results, that most experienced participants now treat every new launch as guilty until proven innocent. Teams vanish. Treasuries drain. Governance devolves into whale-dominated theater.

Futard.io, built by the MetaDAO team on Solana, claims to have a structural answer. Instead of trusting founders with raised capital, the platform locks funds in smart contract escrow and uses prediction markets to govern how that capital gets spent. The idea borrows from economist Robin Hanson’s futarchy concept, first formalized around the year 2000: let markets, not votes, determine which decisions create value.

It is an interesting experiment. It is also far more fragile than its marketing suggests. This piece examines the design, the economics, the risks, and the open questions that anyone participating should understand before committing a dollar.

What the Platform Actually Does

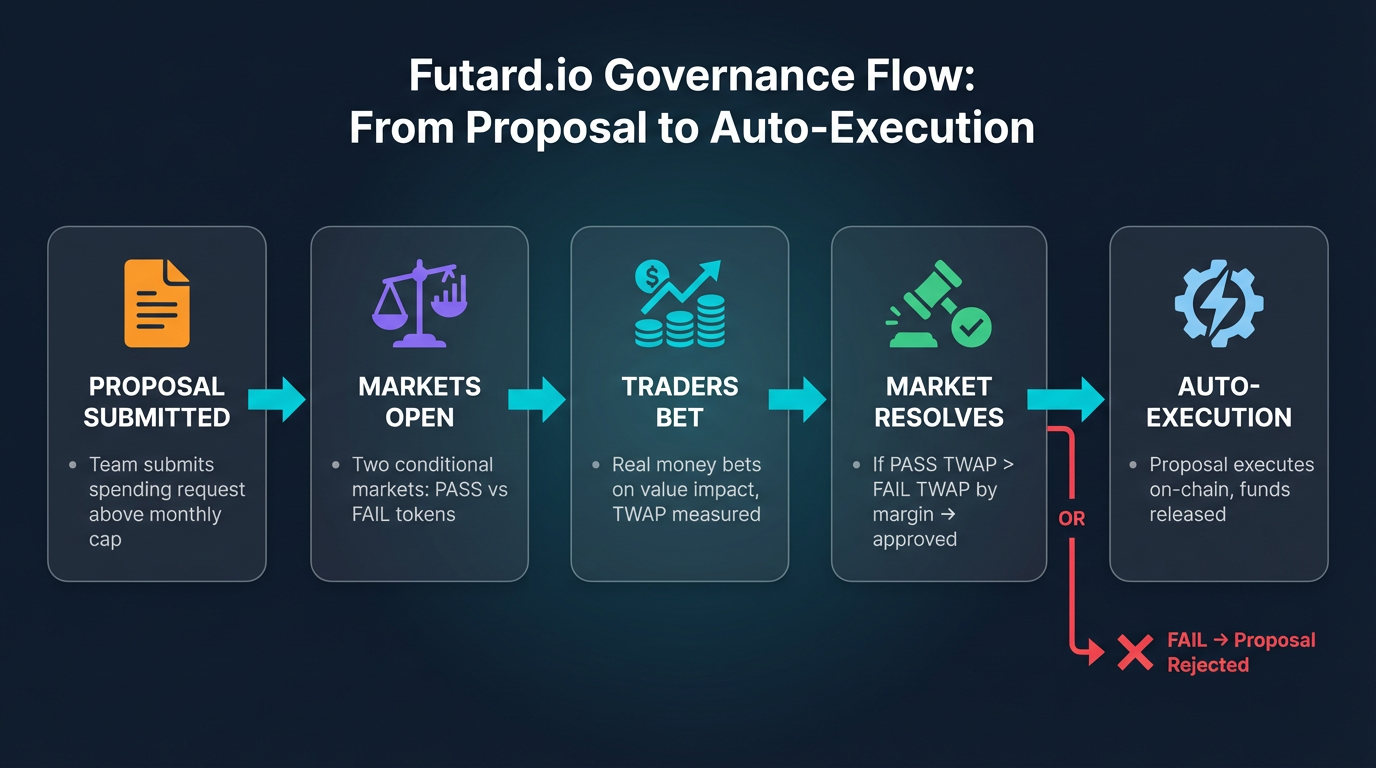

Here’s how it works. A builder pays 1 SOL to deploy a raise through a guided form, setting a fundraising target between $50K and $500K in USDC, a monthly spending limit, and at least three distinct treasury wallets. Contributors commit USDC into escrow smart contracts. If the raise hits its goal, tokens distribute and a futarchy-governed DAO spins up immediately. If it doesn’t, contributors get a full refund.

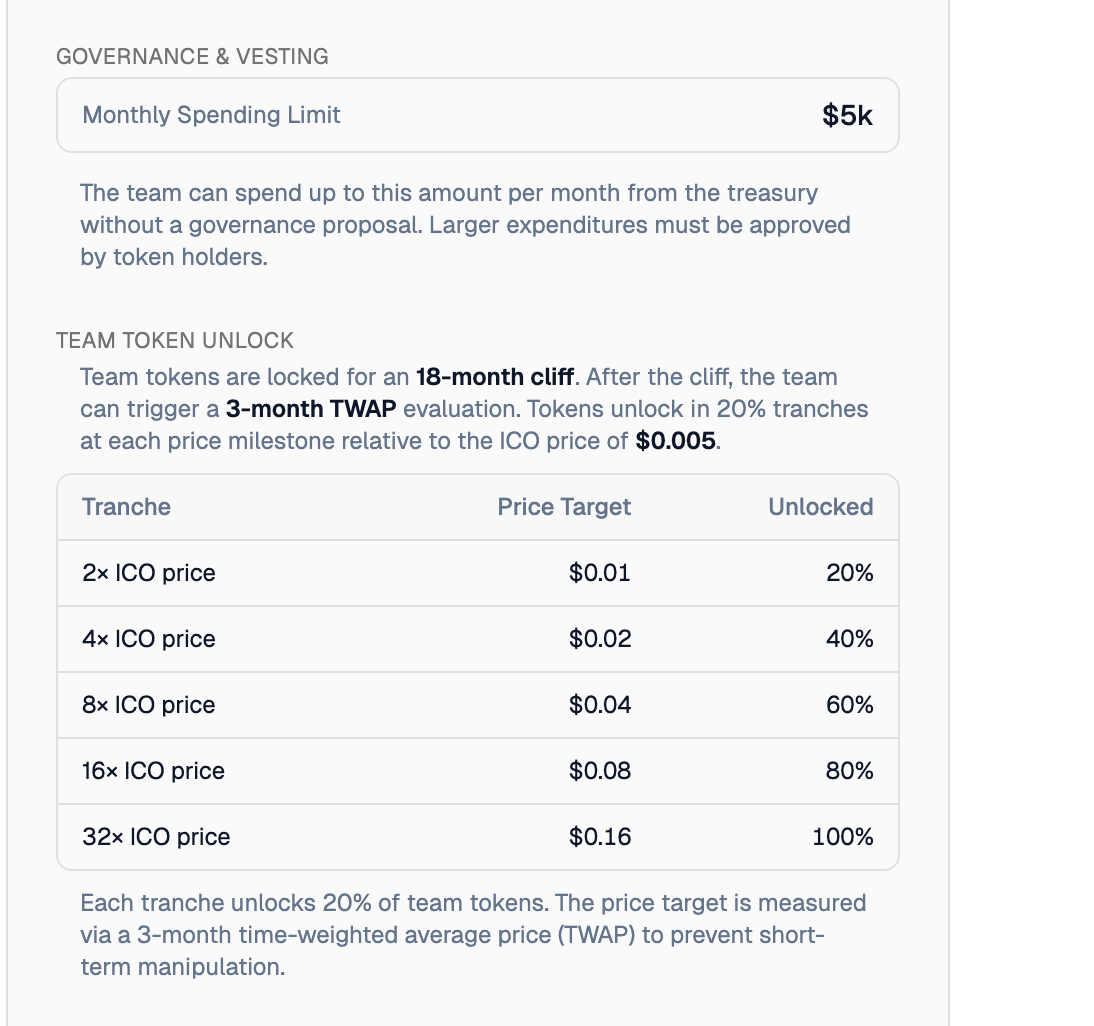

Post-raise, the team can only access funds up to a pre-set monthly cap without market approval. Want to spend above that cap? Submit a proposal. Two conditional prediction markets open, one for “pass” and one for “fail.” Traders bet real money on whether the proposal will increase or decrease the token’s value. If the time-weighted average price of PASS tokens exceeds FAIL tokens by a defined margin, the proposal executes automatically.

As of early 2026, MetaDAO’s platform has facilitated over $33 million in cumulative raises across 10 launched projects, with active raises spanning open-source wallets, privacy infrastructure, real-world asset plays, and even a self-referential futarchy-governed memecoin.

The Allocation Mechanism and Its Tradeoffs

Futard uses time-weighted allocation for token distribution. The formula blends committed capital with how early you commit. Early believers receive a larger share of the token supply at the same fully diluted valuation.

This rewards conviction and discourages last-second sniping, which is a real problem on other launchpads. But it also creates a familiar asymmetry. Early participants often have less information than late participants. Someone committing on day one is making a bet with less data than someone committing on day fourteen, who may have watched community reaction, analyzed the tokenomics more carefully, or seen technical progress. Yet the late participant gets penalized with a worse allocation.

In effect, the mechanism replaces one form of insider advantage (VC pre-sales) with another (early-commitment advantage). Whether this is better depends on your assumptions about who tends to commit early and why.

The Treasury Escrow: What It Solves and What It Doesn’t

The single most valuable design choice in Futard has nothing to do with futarchy. It’s the treasury escrow.

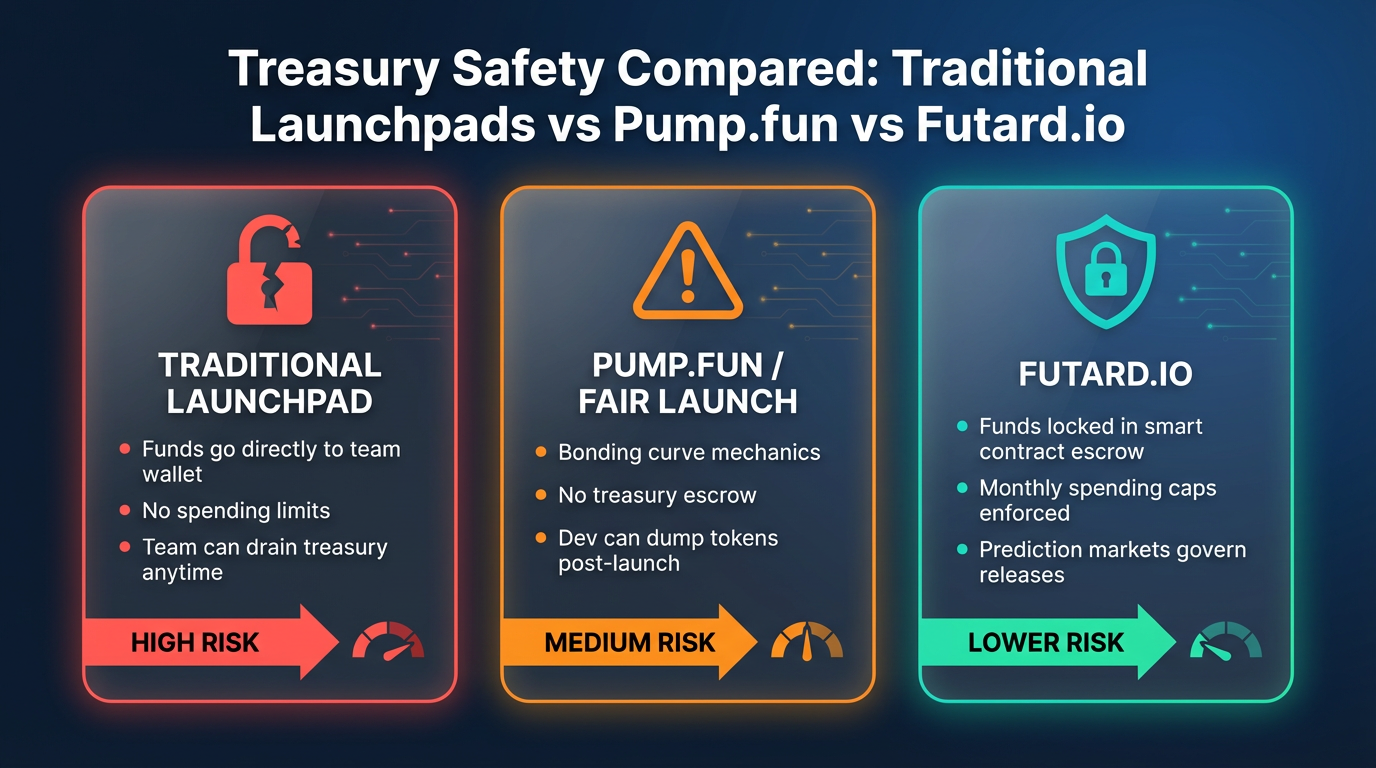

On most launchpads, raised funds flow directly into team wallets. The team can, at any point, drain the treasury and disappear. This happens constantly. Futard’s escrow model throttles capital release through smart contracts and monthly spending caps, which removes the most common rug pull vector entirely.

This is a meaningful structural improvement. But it’s worth being precise about what “unruggable” actually means here, and where the claim breaks down.

Smart contract custody is not the same as economic safety. A team cannot steal the treasury in one transaction, true. But they can propose spending, frame proposals favorably, and extract value through legitimate-looking channels: salaries, vendor payments, marketing budgets routed through related entities, or grants to friendly parties. Prediction markets are supposed to catch these bad proposals, but prediction markets are not omniscient. They’re only as good as the information, liquidity, and participation they attract.

Futarchy: The Interesting Part, and the Most Fragile

Robin Hanson proposed futarchy over two decades ago. The core thesis is elegant: democratic processes are decent at expressing values (what people want), but poor at aggregating information (what policies will achieve those values). Markets, by contrast, excel at information aggregation because participants put money behind their beliefs.

Hanson’s slogan captures it well: “Vote on values, bet on beliefs.”

MetaDAO brought this from theory to practice on Solana, first for its own governance, then as “Futarchy as a Service” for projects like Drift, Jito, and Sanctum. Futard extends this model to every project launched on the platform.

The concept works beautifully in theory. In practice, several structural problems remain unresolved.

The Liquidity Problem

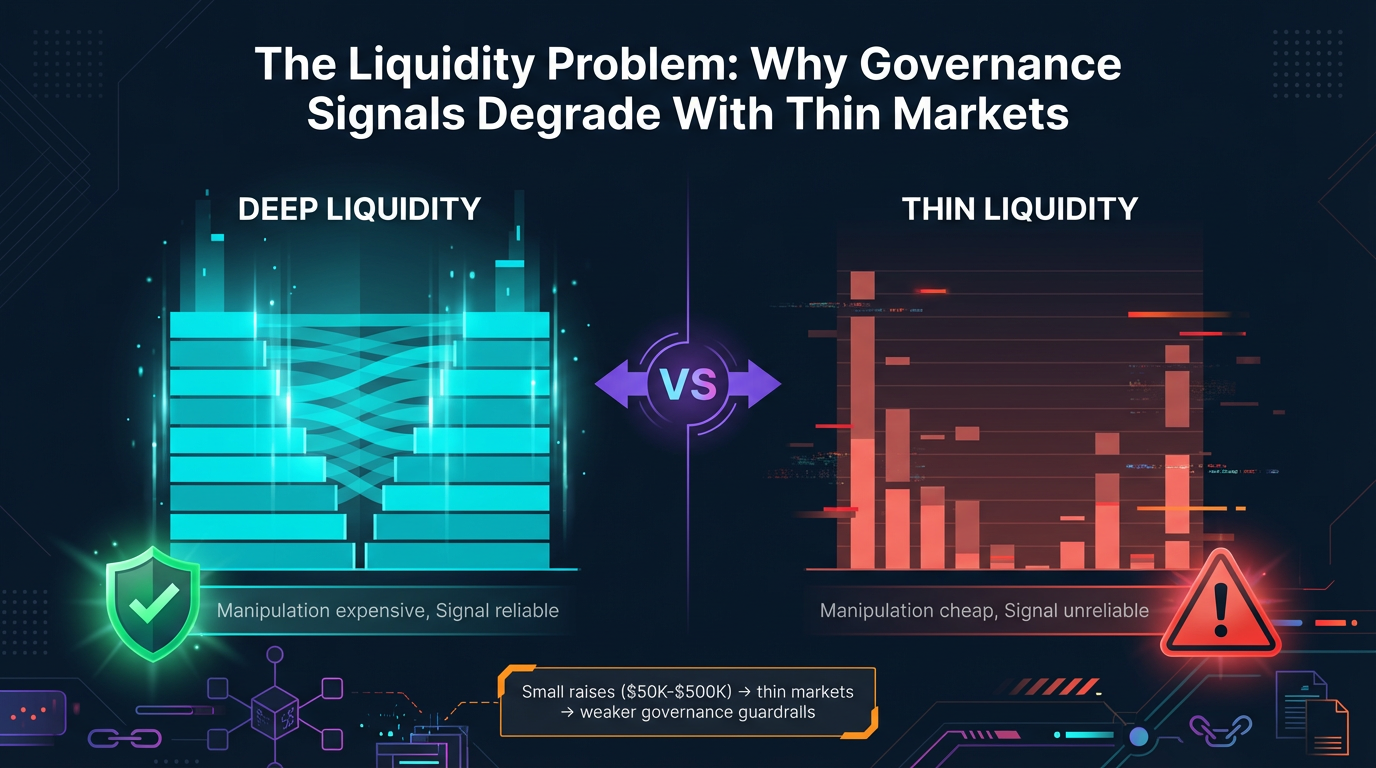

Prediction markets produce useful signals only when they attract enough traders with enough capital to make manipulation expensive. Deep, liquid markets are hard to manipulate because pushing the price in one direction creates profitable opportunities for informed traders to push it back.

Small projects raising $50K to $500K will almost certainly not generate deep prediction markets. A handful of traders, thin order books, and wide spreads are the likely reality. In these conditions, the cost of manipulating a governance outcome might be trivially small relative to the treasury at stake.

Consider: if pushing the PASS market costs $5K but unlocks a $50K treasury disbursement, the manipulation is profitable. The system fails precisely when it matters most. The small, early-stage projects that form the bulk of Futard’s current pipeline are the ones most vulnerable.

The Information Asymmetry

Founders know more than traders. They know the actual state of development, the health of their finances, the status of partnerships, and their real intentions. Markets can only price information that’s publicly available or credibly inferred.

This recreates the same asymmetry that plagues public equities and traditional DAO voting. Insider knowledge advantages the proposer. The futarchy model doesn’t eliminate this, it just moves the venue from a governance vote to a prediction market.

Token Price as the Governance Metric

The design assumes token price is a reasonable proxy for project health. This assumption deserves more scrutiny than it typically gets.

Token prices respond to speculation, liquidity conditions, market cycles, and narrative as much as they respond to fundamentals. A proposal to execute a massive token buyback might pump the price temporarily while draining the treasury. Markets might approve decisions that look good for price in the short term but damage the project’s long-term viability.

Tyler Cowen, the economist, has argued that values and beliefs cannot be cleanly separated in the way futarchy requires. The token price metric carries implicit value judgments about what “success” means, and those judgments may not align with long-term health.

The Governance Fatigue Problem

Futarchy demands continuous participation. Every spending proposal triggers a market. Participants must analyze proposals, trade conditional tokens, and monitor outcomes. This is cognitively expensive, and most people won’t do it consistently.

The likely result is that governance drifts toward a small group of sophisticated traders who actively monitor and trade these markets. This isn’t necessarily worse than whale-dominated token voting, but it does recreate a concentrated decision-making class, just a different one. Instead of large token holders calling the shots, a handful of active market participants steer governance.

Sanctum co-founder FP Lee acknowledged this adoption friction when he told Blockworks that MetaDAO needs “one great success” for broad adoption. MetaDAO’s own pseudonymous founder has admitted that the friction of learning how futarchy works has been higher than expected.

The Cayman SPC and the Decentralization Tension

Futard requires projects to form a Cayman Islands SPC entity through MetaLeX. This adds a real-world legal wrapper, jurisdiction, compliance obligations, and regulatory exposure.

There’s nothing wrong with legal structure per se. But it sits awkwardly against the “permissionless” narrative. The platform is designed to be legally defensible, not purely decentralized. This is probably the right call for longevity, but participants should understand what they’re getting: a hybrid system with real-world legal hooks, not a purely trustless protocol.

The $500K Cap Tells a Story

Raise caps exist for a reason. If the governance model were robust at scale, there would be no need to limit raises to $500K.

The cap almost certainly reflects the reality that prediction markets are thin at this stage, governance mechanisms are experimental, and the potential for damage needs to be bounded. This is prudent engineering. But it also means Futard is, for now, an experimental sandbox rather than a scalable capital formation system.

The Memecoin Contradiction

Among the active raises, projects like “Futardio Cult,” a futarchy-governed memecoin, highlight an internal tension. Memecoins thrive on speed, narrative, and speculative energy. Futarchy governance requires careful analysis, market depth, and informed trading. These cultures don’t obviously mix well.

If governance markets on memecoin DAOs attract participants who treat them as speculative instruments rather than deliberative mechanisms, the governance signal degrades. The market becomes a game rather than an information aggregation tool.

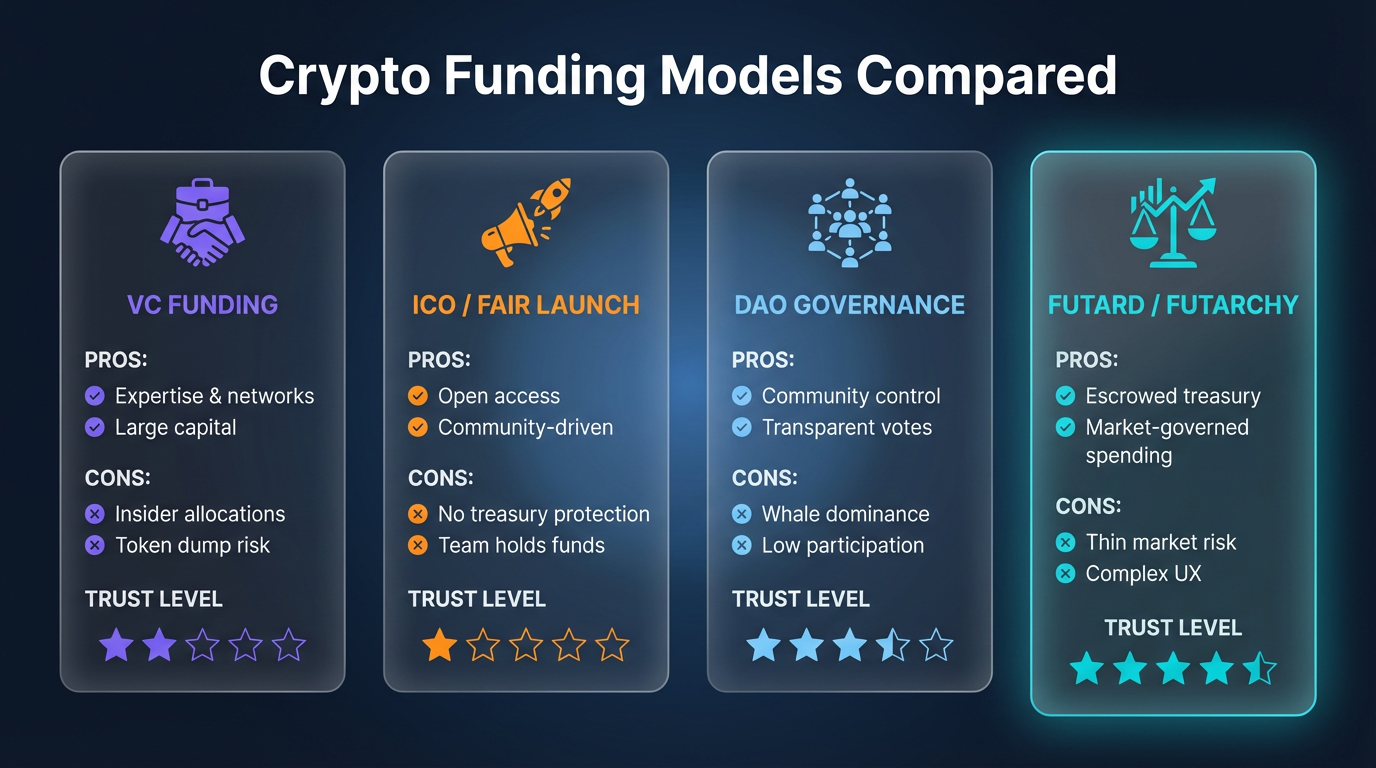

Where This Fits Among Other Funding Models

Every crypto funding model involves tradeoffs:

- VC funding provides expertise and networks but creates insider allocations and token-dumping incentives.

- ICOs and fair launches offer open access but leave treasuries in team hands.

- Futard’s model introduces treasury safeguards and structured governance, but at the cost of complexity, liquidity risk, and experimental economics.

The honest comparison isn’t “Futard vs. a perfect launchpad.” It’s “Futard vs. the status quo,” which includes platforms where rugs are routine and governance is nonexistent. On that curve, Futard is a clear improvement. The treasury escrow alone justifies attention.

What Would Success Look Like?

If this experiment works, we’d expect to see several things: projects shipping real products after raising through the platform, prediction markets with enough liquidity to resist cheap manipulation, treasury spending that demonstrably aligns with outcomes, and governance participation from people beyond a small insider circle.

Without those signals, the most likely outcome is that Futard becomes a valuable governance research platform, useful for the handful of crypto-native builders who appreciate its structure, but not a mainstream capital formation tool. That’s still valuable. Not everything needs to be mainstream to matter.

The Bottom Line

Futard.io combines a good idea (escrowed treasuries with spending limits) with an ambitious one (futarchy governance). The first part works well today. The second part is an open experiment with unresolved questions about liquidity, information asymmetry, and metric design.

The promotional framing around the platform, “unruggable,” “markets guard your money,” overstates the current reality. Markets guard your money only if those markets are deep, liquid, and well-informed. On small raises with thin prediction markets, the guardrails are weaker than the branding implies.

That said, the fact that anyone is trying this at all matters. Robin Hanson proposed futarchy more than 25 years ago, and real-world implementations have been vanishingly rare. MetaDAO’s work on Solana, with Paradigm’s backing and adoption by projects like Drift and Sanctum, represents the most serious attempt to date. Whether it scales beyond a niche governance experiment depends on whether the early projects deliver results that make the learning curve worth climbing.

For now, treat Futard as what it is: experimental governance infrastructure built on sound principles, constrained by the realities of thin markets and early adoption. Participate with that understanding, and you’ll be making a more informed bet than most people in crypto ever do.