Roughly an hour ago, the SEC published a 68-page interpretive release that does something the crypto industry has waited over a decade to see: it explains, in detail, how the Commission plans to apply securities law to crypto assets and core DeFi activities going forward. The CFTC joined the document to provide its own guidance stating it will administer the Commodity Exchange Act consistently with the SEC’s interpretation. Both agencies appear as co-authors, but the interpretation itself is the SEC’s. The CFTC’s role is alignment, not co-authorship of the legal analysis.

The release is titled Application of the Federal Securities Laws to Certain Types of Crypto Assets and Certain Transactions Involving Crypto Assets (Release Nos. 33-11412 and 34-105020). It was announced by SEC Chairman Paul Atkins at the DC Blockchain Summit today, with CFTC Chairman Michael Selig speaking from the same stage. Atkins’ headline soundbite: “Most crypto assets are not themselves securities.”

That’s a powerful framing from the chairman, but it’s his characterization in a speech, not the release’s legal holding. The release itself is more measured. It classifies crypto assets into categories, explains when the Howey test does and doesn’t apply, and walks through specific activities like staking and airdrops. It doesn’t declare a blanket rule. It offers the Commission’s interpretive view, grounded in nearly 80 years of investment contract case law, of how existing securities law maps onto crypto.

The details are where the real value is. Let’s get into them.

The five-bucket taxonomy: useful, but interpretive

The SEC classifies crypto assets into five categories. Only one of them, digital securities, falls under full SEC jurisdiction. The rest, under the Commission’s interpretation, sit outside the securities framework or under CFTC oversight.

Digital commodities are crypto assets intrinsically linked to the programmatic operation of a “functional” crypto system. Their value comes from network operation and supply-demand dynamics, not from the managerial efforts of a central team. The release goes further than describing abstract criteria. It names 16 specific assets and concludes, at the Commission level, that each qualifies as a digital commodity: Aptos (APT), Avalanche (AVAX), Bitcoin (BTC), Bitcoin Cash (BCH), Cardano (ADA), Chainlink (LINK), Dogecoin (DOGE), Ether (ETH), Hedera (HBAR), Litecoin (LTC), Polkadot (DOT), Shiba Inu (SHIB), Solana (SOL), Stellar (XLM), Tezos (XTZ), and XRP (XRP). The footnote clarifies that these were selected as examples because each underlies a futures contract trading on a CFTC-regulated market, but adds that having such a futures contract is not required. It even names Algorand (ALGO) and LBRY Credits (LBC) as additional examples that qualify despite lacking futures contracts. This is more concrete than most people expected. It’s an interpretive conclusion, not a statutory designation, but it’s the Commission itself saying these assets meet its criteria, based on its understanding of their characteristics as of today’s date.

Digital collectibles cover NFTs, meme coins, cultural tokens. Things people buy because they want to own them, not because they expect a team to make the number go up.

Digital tools are utility tokens with a specific function, like ENS domains or soulbound credentials. Pure function, no investment thesis.

Stablecoins get their own lane. Payment stablecoins under the GENIUS Act (signed July 2025) are carved out by statute. Others get analyzed case-by-case.

Digital securities are tokenized stocks, bonds, revenue-sharing instruments, and anything else that meets the definition of a security whether it lives on a blockchain or not.

A crucial caveat that most early coverage is glossing over: this is an interpretive release, not a statute or a formal rule. The release itself says it “does not supersede or replace the Howey test, which is binding legal precedent.” It also explicitly invites public comment and says the Commission may “refine, revise, or expand upon the interpretation.” That’s not the language of settled law. It’s the Commission telling you how it currently plans to apply existing law, which carries real weight in practice (especially for enforcement discretion) but is not the same as a safe harbor, a no-action letter, or a statute. A future Commission could revise it. A court could disagree with it.

Staking gets a framework. Read the fine print.

This is the section that matters most for anyone running or using a DeFi protocol today.

The SEC’s interpretation addresses what it calls “protocol staking,” and its conclusion is favorable: protocol staking activities, in the manner and under the circumstances described in the interpretation, do not involve the offer and sale of a security. The release uses language drawn from decades of case law, characterizing staking as an “administrative or ministerial activity” rather than the kind of “essential managerial efforts” that trigger Howey. That ministerial/managerial distinction isn’t the SEC’s invention. It cites Eighth Circuit and Sixth Circuit precedent, plus a 2025 Southern District of New York decision, establishing that ministerial tasks don’t satisfy the “efforts of others” prong.

The release covers four configurations explicitly: self (solo) staking, self-custodial staking with a third-party node operator, custodial staking, and liquid staking. In each case, the Commission’s reasoning is the same. The staker or their agent is performing administrative functions to secure a PoS network. Rewards flow from the protocol’s rules, not from a promoter’s business activities. No investment contract is formed.

The release also addresses ancillary services that staking providers commonly offer: slashing coverage, early unbonding, alternate reward payment schedules, and aggregation of digital commodities to meet minimum staking thresholds. All of these are classified as administrative or ministerial. They don’t convert the staking relationship into a securities transaction.

The practical read for protocols like Lido, Rocket Pool, and Jito is positive. Staking receipt tokens (LSDs) get their own subsection. A receipt token for a non-security crypto asset that is not subject to an investment contract is itself not a security and not a derivative. It’s a receipt. Trading them on DEXs, using them as collateral, bridging them, none of that triggers registration requirements under this interpretation.

But the release is precise about where the line sits. Three explicit carve-outs appear in the footnotes: if a custodian selects whether, when, or how much of a depositor’s assets to stake, that’s outside the interpretation’s scope. If a liquid staking provider does the same, outside scope. And if any provider guarantees or sets the amount of rewards, outside scope. The distinction between acting as a ministerial agent and exercising discretionary judgment is the boundary. Cross it and you’re back in Howey territory.

Wrapping and bridges: the quiet win

Wrapped tokens got less attention in the early coverage, but the release dedicates a full section (Section VI) to them with a clear conclusion.

The interpretation covers what it calls “Redeemable Wrapped Tokens,” issued when a person deposits a crypto asset with a custodian or cross-chain bridge and receives an equivalent token on a different network or standard. The conditions: one-for-one backing, redeemable on a fixed one-for-one basis (at which point the wrapped token is burned), and the deposited asset is locked up and cannot be transferred, lent, pledged, or rehypothecated.

Under those conditions, the wrapped token is a receipt, not a security. The Commission’s reasoning: no investment in an enterprise is being made, the deposited assets aren’t pooled for deployment by promoters, and the wrapping process itself is administrative or ministerial. The Wrapped Token Provider isn’t generating returns, there’s no financial incentive beyond the underlying asset’s value.

For WETH, WBTC, and their equivalents across chains, this is strong footing. Cross-chain composability, bridge operations, and wrapped-asset liquidity pools all become more defensible for U.S. users and builders.

The important qualifier: wrapped tokens that are receipts for digital securities or for non-security crypto assets subject to an investment contract are themselves securities. The wrapping doesn’t launder the underlying asset’s status.

Airdrops: better footing, but narrower than you think

The SEC’s interpretation addresses airdrops, and the conclusion is favorable for many common structures. But the scope is tighter than the headline coverage suggests.

The interpretation covers airdrops of non-security crypto assets where recipients do not provide the issuer with money, goods, services, or other consideration in exchange for the airdropped tokens. Under those conditions, the first prong of Howey (investment of money) is not met, so no investment contract is formed.

That covers some important scenarios. The release gives three specific examples: snapshot-based drops where the issuer doesn’t announce the airdrop beforehand, retroactive rewards for prior testnet usage announced only after the qualifying period, and drops to application users based on past activity with no pre-announcement.

But here’s what’s explicitly excluded: airdrops where the recipient performs a task in exchange for the tokens. The release lists examples like retweeting, writing articles, referring users, or fixing bugs. If those tasks are bargained-for consideration for the airdrop, the interpretation doesn’t apply. That cuts out a meaningful portion of what the industry casually calls “airdrops,” as many programs require recipients to complete social tasks, hold minimum balances, or interact with specific contracts to qualify.

There’s also a key footnote (146) that many will miss: even if the airdrop itself doesn’t create an investment contract, the airdropped tokens could become subject to one through subsequent transactions. If a separate investment contract already exists around that token (from a prior sale, for example), selling the airdropped tokens in secondary markets could constitute a securities transaction.

The net effect: truly free, no-strings-attached community drops are on solid ground. Task-based airdrop campaigns, questing programs, and drops that require ongoing engagement in exchange for tokens need more careful analysis.

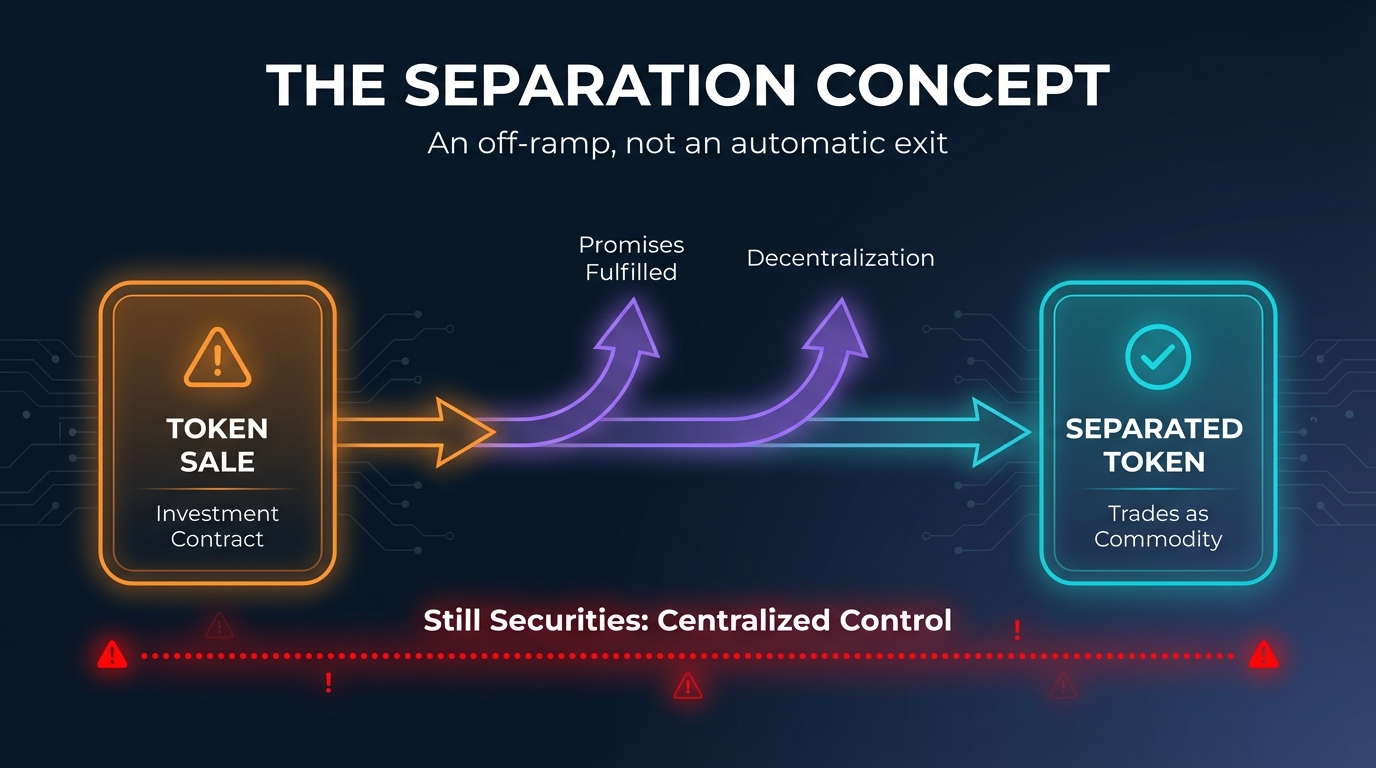

The separation concept: an off-ramp, not an automatic exit

This might be the most underappreciated piece of the release, and also the most likely to be misunderstood.

The SEC’s interpretation addresses how a non-security crypto asset can “cease to be subject to” an investment contract. Section IV.B describes two paths. First, the issuer fulfills its representations or promises to undertake essential managerial efforts. Once those efforts are complete, purchasers no longer have reasonable expectations of profits from the issuer, and the investment contract ceases to exist. Second, the issuer fails to satisfy its promises, either through abandonment, inability, or simply enough time passing that no reasonable person would still expect the issuer to deliver. In that case too, the investment contract terminates.

This is genuinely new territory. Under the Gensler-era SEC, once a token was caught in an investment contract analysis, there was no articulated way out. Projects lived in permanent limbo. The interpretation now provides a conceptual off-ramp.

But “conceptual off-ramp” is not “automatic exit.” The release is clear that how separation works depends on how the issuer itself defined its commitments. If you promised decentralization, whether you’ve achieved it is measured against your definition, not a general market conception. If you promised functionality milestones, the standard is your own roadmap. The release also emphasizes that separation doesn’t erase past violations. If the original offering should have been registered but wasn’t, that liability survives even if the token later separates from the investment contract.

There’s also a practical detail: the release says the issuer should “publicly disclose the completion of those efforts.” Until the issuer communicates that it’s done, purchasers may still reasonably expect ongoing effort. Separation requires affirmative signaling, not just quiet completion.

Expect this concept to become one of the most negotiated aspects of the framework. Every project that raised funds through a token sale and subsequently decentralized will be looking at this provision and asking: are we separated yet? The honest answer for most of them is “maybe, and you’ll need a legal opinion benchmarked against your own prior representations.”

What this actually means for the market

Let’s move past the legal analysis and talk about what happens next.

Institutional capital has fewer excuses. The biggest barrier to TradFi money entering DeFi wasn’t yield. It was legal uncertainty. When your compliance team can’t definitively say whether staking ETH is a securities transaction, you don’t stake ETH. This interpretation materially reduces that uncertainty for the largest assets and most common activities. Expect staking inflows from institutional custodians, asset managers, and the growing number of crypto ETFs that can now integrate staking into their products, though each will need its own legal analysis of whether it fits the described circumstances.

U.S. builders can stop pretending to be offshore. The regulatory exile of American DeFi founders, incorporating in the Caymans while operating from Denver, was always absurd. This release gives U.S.-based protocols a framework to build under. Talent and venture capital that migrated to Singapore and Dubai may start flowing back.

Altcoin ETFs get closer. With the SEC’s interpretation explicitly concluding that SOL, XRP, ADA, AVAX, DOT, and others are digital commodities, the path to spot ETFs for assets beyond BTC and ETH shortens materially. The SEC already approved listing standards for commodity-based trust shares in 2025 that allow Nasdaq, NYSE Arca, and Cboe to list qualifying products without asset-specific filings. The interpretive conclusion isn’t a statutory designation, but it removes the ambiguity that was the primary obstacle. The CFTC’s commodity framework for these assets still needs development, but the securities-law question is now largely answered for the named tokens.

Composability gets more defensible. The DeFi stack, DEXs, lending protocols, perpetuals, options, all built on layers of staking, wrapping, and bridging, can now operate with a clearer regulatory basis rather than as a collection of legal gray areas. Uniswap, Aave, and newer protocols built on LSDs and wrapped collateral are the obvious beneficiaries.

What this doesn’t fix

It’s worth being precise about the limits.

Promissory language still kills you. If your whitepaper, your Twitter account, or your Discord mods are promising profits from the team’s ongoing work, the Howey test still applies. The release is generous to decentralized systems, not to projects that call themselves decentralized while operating like startups.

Centralized control is still the red line. If a team retains operational, economic, or voting control over the protocol, the token may remain subject to an investment contract. The taxonomy rewards actual decentralization, not branding.

Antifraud rules apply everywhere. Nothing in this release immunizes anyone from fraud liability. Pump-and-dump schemes, material misrepresentations, failure to deliver on stated functionality, all of that still triggers enforcement. AML, tax, and state-level regulations remain in force.

Digital securities are still fully regulated. Tokenized RWAs representing equity, debt, or revenue-sharing are securities. Full stop. The release addresses compliant tokenization, but it doesn’t exempt anything that is actually a financial instrument from registration.

The CFTC now has work to do. Commodities oversight of crypto is the CFTC’s domain, and the agency is far less developed in its crypto rulemaking than the SEC. The coordination between the two agencies via Project Crypto is a start, but there’s a gap between “this is a commodity” and “here’s how commodity markets in this asset should work.” That gap will take time to fill.

Restaking is explicitly not addressed. The release contains a footnote (107) stating it “does not address ‘restaking,’ which is a process that allows digital commodities staked on their associated crypto network to be used on additional crypto systems.” EigenLayer and the broader restaking ecosystem remain in uncharted regulatory territory.

The bigger picture

This release is the first major deliverable of Project Crypto and the SEC’s Crypto Task Force. It aligns with the GENIUS Act, the CFTC’s Crypto Sprint, and the broader post-2024 regulatory reset. It reflects a White House that has repeatedly called for America to be “the crypto capital of the world,” and an SEC chairman who told the DC Blockchain Summit today that the agency is “not the securities and everything commission anymore.”

The practical question is how fast the ecosystem adapts. The Commission’s interpretive view is now public. It’s detailed enough to act on, but it’s not the final word. The release itself invites public comment and says the Commission may refine, revise, or expand upon the interpretation. This is the Commission’s first step, by its own description, not the last.

One thing worth watching: the release is an interpretation, not a statute or a formal rule. It carries real weight, especially because the Commission says it will administer the securities laws consistently with it, including for enforcement. But it can be superseded by future rulemaking, revised by a future Commission, or contradicted by a court. The CLARITY Act, which would codify a comprehensive market structure framework, is still stalled in Congress. If it passes, it may modify or extend what the SEC laid out today. If it doesn’t, this interpretation becomes the strongest guidance available, but it remains guidance, not law.

For builders, users, and LPs

If you’re building a protocol: audit your communications. Strip out profit promises. Document your decentralization milestones. Get a legal opinion on whether your token qualifies as a digital commodity under this framework. If it does, you have a strong interpretive basis to work from. If it doesn’t, the release tells you what the Commission is looking for.

If you’re a user: stake, swap, wrap, and farm on major chains with the understanding that the SEC’s interpretation treats these activities favorably under the described circumstances. This doesn’t make you risk-free, but it materially reduces the regulatory cloud that hung over yield-bearing DeFi strategies.

If you’re providing liquidity or running a validator: the ministerial/administrative classification works in your favor, provided you aren’t exercising discretion over client assets or making profit guarantees. Stay within the described parameters and the interpretation is on your side.

The fog lifted substantially today. Not through a vague speech or a footnote in an enforcement settlement. Through 68 pages of detailed interpretive guidance from the Commission, with the CFTC aligned alongside it.

But interpretive guidance is not statute, and the release itself acknowledges this is a first step. What it gives the market is the SEC’s current view, articulated with unusual specificity and detail, of how existing securities law applies to the core activities of DeFi. That’s not everything the industry wanted. It’s a lot more than it had yesterday.